Fluctuations in economic activity (economic conditions), consisting in repeated contraction (economic recession, recession, depression) and expansion of the economy (economic recovery). The cycles are periodic, but usually irregular. Usually (within the framework of the neoclassical synthesis) they are interpreted as fluctuations around a long-term trend in the development of the economy.

The deterministic view of the causes of economic cycles comes from predictable, well-defined factors that are formed at the stage of recovery (decline factors) and recession (rise factors). The stochastic point of view proceeds from the fact that cycles are generated by factors of a random nature and represent a reaction economic system to internal and external impulses.

Usually isolated four main types economic cycles:

short-term Kitchin cycles(characteristic period - 2-3 years);

medium term Juglar cycles(characteristic period - 6-13 years);

Kuznets rhythms (characteristic period - 15-20 years);

long Kondratieff waves(typical period - 50-60 years).

Phases

There are four relatively distinct phases in business cycles: peak, decline, bottom (or "trough"), and rise; but in nai more these phases are characteristic of Juglar cycles.

Business cycles in economics

Climb

The rise (revival) occurs after reaching the lowest point of the cycle (bottom). It is characterized by a gradual increase in employment and production. Many economists believe that this stage is not inherent in high rates inflation. There is an introduction of innovations in the economy with short term payback. Demand deferred during the previous recession is realized.

Peak

The peak, or top of the business cycle, is the "high point" of an economic expansion. In this phase, unemployment usually reaches the lowest level or disappears completely, production capacities operate at maximum or close to it, that is, almost all material and material resources available in the country are involved in production. labor resources. Usually, though not always, inflation rises during peaks. The gradual saturation of markets increases competition, which reduces the rate of return and increases the average payback period. The need for long-term lending is growing with a gradual decrease in the ability to repay loans.

recession

Recession (recession) is characterized by a reduction in production volumes and a decrease in business and investment activity. As a result, unemployment increases. Officially, a downturn, or recession, is defined as a downturn in business activity that lasts more than three consecutive months.

Bottom

The bottom (depression) of the economic cycle is the "lowest point" of production and employment. It is believed that this phase of the cycle is usually not long. However, history knows exceptions to this rule. The Great Depression of the 1930s, despite periodic fluctuations in business activity, lasted 10 years (1929-1939).

A characteristic feature of cyclic development is that it is, first of all, development, and not fluctuations around a certain constant (potential) value. Cyclicity means development in a spiral, and not in a vicious circle. This mechanism of the progressive movement in its various forms. In the economic literature, it is emphasized that cyclical fluctuations occur around the trajectory of long-term growth (secular trend).

Causes

The theory of real economic cycles explains recessions and booms by the influence of real factors. In industrialized countries, this may be the emergence of new technologies, changes in prices for raw materials. In agricultural countries - harvest or crop failure. Also, force majeure situations (war, revolution, natural disasters) can become an impetus for change. Anticipating a change in the economic environment for better or worse, households and firms massively start saving or spending more. As a result, aggregate demand decreases or increases, turnover decreases or increases. retail. Firms receive fewer or more orders for the manufacture of products, respectively, the volume of production, employment changes. Business activity is changing: firms begin to reduce the range of products or, on the contrary, launch new projects, take loans for their implementation. That is, the entire economy fluctuates, trying to come to equilibrium.

In addition to fluctuations in aggregate demand, there are other factors that affect the phases of the economic cycle: changes that depend on the change of seasons in agriculture, construction, automotive industry, retail seasonality, secular trends economic development countries dependent on the resource base, the size and structure of the population, good governance.

Impact on the economy

The existence of the economy, as a set of resources for steadily growing consumption, is oscillatory. Fluctuations in the economy are expressed in the economic cycle. The “thin” moment of the economic cycle is considered to be a recession, which, at some scale, can turn into a crisis.

The concentration (monopolization) of capital leads to "erroneous" decisions on the scale of the economy of the country or even the world. Any investor seeks to receive income from his capital. The investor's expectation of this return comes from the boom-peak stage, when returns are at their highest. At the stage of recession, the investor considers it unprofitable for him to invest in projects with a yield lower than “yesterday”.

Without such investments (investments), production activity is reduced, as a result, the solvency of workers in this area, who are consumers of goods and services in other areas. Thus, the crisis of one or several industries is reflected in the entire economy as a whole.

Another problem of capital concentration is withdrawal money supply(money) from the sphere of consumption and production of consumer goods (also the sphere of production of the means of production of these goods). Money received in the form of dividends (or profits) is accumulated in the accounts of investors. There is a shortage of money to maintain the required level of production, and as a result, a decrease in the volume of this production. The unemployment rate is growing, the population is saving on consumption, and demand is falling.

Of the sectors of the economy, the services and non-durable goods sectors are somewhat less affected by the devastating effects of the economic downturn. The recession is even boosting some activities, such as boosting demand for pawnshops and bankruptcy lawyers. Firms that produce capital goods and consumer durables are most sensitive to cyclical fluctuations.

These firms are not only the hardest hit in the downturn, but also the most benefit from the recovery in the economy. There are two main reasons:

- the possibility of postponing purchases;

- market monopolization.

Purchase capital equipment most often can be postponed to the future; in difficult times for the economy, manufacturers tend to refrain from purchasing new machinery and equipment and building new buildings. During an extended downturn, firms often choose to repair or upgrade outdated equipment rather than spend heavily on new equipment.

As a result, investment in capital goods declines sharply during economic downturns. The same applies to consumer durables. Unlike food and clothing, buying a luxury car or an expensive household appliances can be postponed until better times. During economic downturns, people are more likely to repair rather than replace durable goods. Although food and clothing sales tend to decline as well, the decline is usually smaller than the decline in demand for durable goods.

Monopoly power in most industries producing capital goods and consumer durables is due to the fact that the markets for these goods are usually dominated by a few large firms. Their monopoly position allows them to keep prices steady during economic downturns by reducing production in response to falling demand. Consequently, the fall in demand has a much greater impact on production and employment than on prices. A different situation is typical for industries that produce consumer goods. When demand falls, these industries usually respond by lowering prices in general, since no single firm has significant monopoly power.

History and long cycles

Business cycles are not truly "cyclical" in the sense that the length of the period from, say, peak to peak has fluctuated considerably throughout history. Although economic cycles in the United States lasted an average of about five years, cycles have been known to last from one to twelve years. The most pronounced peaks (measured as a percentage increase above the economic growth trend) coincided with the great wars of the 20th century, and the deepest economic recession, excluding the Great Depression, was observed after the end of the First World War.

Late 20th century American economy appears to have entered a period of prolonged decline, as evidenced by some economic indicators, in particular the level of real wages and net investment. Nevertheless, even with a long-term downward trend in growth, the US economy continues to grow; although the country registered negative GDP growth in the early 1980s, it remained positive in all subsequent years except 1991.

Symptomatic of the long-term downturn that began in the 1960s is the fact that, although growth has rarely been negative, the level of economic activity in the United States since 1979 has hardly ever exceeded the trend growth rate.

It should be noted that along with the described economic cycles, long cycles are also distinguished in theory. Long cycles in the economy - economic cycles with a duration of more than 10 years. Sometimes referred to by the names of their explorers.

Investment cycles(7-11 years old) studied Clement Juglar (fr. Clement Juglar). These cycles, apparently, it makes sense to consider as medium-term rather than long.

Infrastructure investment cycles(15-25 years old) studied by Nobel laureate Simon Kuznets.

Kondratieff cycles(45-60 years old) was described by the Russian economist Nikolai Kondratiev.

It is these cycles that are most often referred to as "long waves" in the economy.

Kitchin cycles

Kitchin cycles- short-term economic cycles with a characteristic period of 3-4 years, discovered in the 1920s by the English economist Joseph Kitchin. Kitchin himself explained the existence of short-term cycles by fluctuations in world gold reserves, but in our time such an explanation cannot be considered satisfactory. In modern economic theory, the mechanism for generating these cycles is usually associated with time delays (time lags) in the movement of information that affect the decision-making of commercial firms.

Firms react to an improvement in the market situation by fully loading capacities, the market is flooded with goods, after some time excessive stocks of goods are formed in warehouses, after which a decision is made to reduce capacity utilization, but with a certain delay, since information about the excess of supply over demand itself usually arrives with a certain delay, in addition, it takes time to verify this information; a certain time is also required to make and approve the decision itself.

In addition, there is a certain delay between the decision-making and the actual reduction in capacity utilization (it also takes time to bring the decision to life). Finally, there is another time lag between when the load level starts to decrease production capacity and actual resorption of excess stocks of goods in warehouses. In contrast to the Kitchin cycles, within the framework of the Juglar cycles, we observe fluctuations not only in the level of utilization of existing production capacities (and, accordingly, in the volume of commodity stocks), but also fluctuations in the volume of investments in fixed capital.

Juglar cycles

Juglar cycles- medium-term economic cycles with a characteristic period of 7-11 years. Named after the French economist Clement Jouglar, one of the first to describe these cycles. In contrast to the Kitchin cycles, within the framework of the Zhuglar cycles, we observe fluctuations not only in the level of utilization of existing production capacities (and, accordingly, in the volume of commodity stocks), but also fluctuations in the volume of investments in fixed capital. As a result, in addition to the time lags characteristic of Kitchin cycles, there are also time delays between the adoption of investment decisions and the construction of the corresponding production facilities (and also between the construction and actual launch of the corresponding facilities).

An additional delay is also formed between the decline in demand and the liquidation of the corresponding production capacities. These circumstances determine that the characteristic period of the Juglar cycles turns out to be noticeably longer than the characteristic period of the Kitchin cycles. Cyclical economic crises/recessions can be considered as one of the phases of the Juglar cycle (along with the phases of recovery, recovery and depression). At the same time, the depth of these crises depends on the phase of the Kondratieff wave.

Since there is no clear periodicity, an average value of 7-10 years was taken.

Phases of the Juglar cycle

In the Juglar cycle, four phases are quite often distinguished, in which some researchers distinguish subphases:

- revival phase (sub-phases of start and acceleration);

- phase of rise, or prosperity (sub-phases of growth and overheating, or boom);

- recession phase (sub-phases of collapse/acute crisis and recession);

- phase of depression, or stagnation (sub-phases of stabilization and shift).

Cycles (rhythms) of Kuznets have a duration of approximately 15-25 years. They are called Kuznets cycles after the American economist, future Nobel laureate Simon Kuznets. They were opened in 1930. Kuznets associated these waves with demographic processes, in particular, the influx of immigrants and building changes, so he called them "demographic" or "building" cycles.

Currently, a number of authors consider Kuznets rhythms as technological, infrastructural cycles. Within these cycles there is a massive upgrade of core technologies. In addition, large cycles in real estate prices coincide well with the Kuznets cycle in the example of Japan 1980-2000. and the duration of the big half-wave of rising prices in the US.

There was also a proposal to consider Kuznets rhythms as the third harmonic of the Kondratiev wave. There is no clear periodicity, so the researchers take an average of 15-20 years.

Kondratieff cycles

Kondratiev cycles (K-cycles or K-waves) are periodic cycles of the modern world economy lasting 40-60 years.

There is a definite relationship between long Kondratiev cycles and medium-term Juglar cycles. Such a connection was noticed by Kondratiev himself. At present, the opinion is expressed that the relative correctness of the alternation of upward and downward phases of the Kondratiev waves (each phase is 20-30 years) is determined by the nature of the group of nearby medium-term cycles. During the upward phase of the Kondratiev wave, the rapid expansion of the economy inevitably brings society into the need for change. But the possibilities of changing society lag behind the requirements of the economy, so development goes into a downward B-phase, during which crisis-depressive phenomena and difficulties force us to rebuild economic and other relations.

The theory was developed by the Russian economist Nikolai Kondratiev (1892-1938). In the 1920s he drew attention to the fact that in the long-term dynamics of some economic indicators there is a certain cyclical regularity, during which phases of growth of the corresponding indicators are replaced by phases of their relative decline with a characteristic period of these long-term fluctuations of about 50 years. Such fluctuations were designated by him as large or long cycles, subsequently named by J. Schumpeter in honor of the Russian scientist Kondratiev cycles. Many researchers began to call them also long waves, or Kondratieff waves, sometimes K-waves.

The characteristic wave period is 50 years with a possible deviation of 10 years (from 40 to 60 years). Cycles consist of alternating phases of relatively high and relatively low economic growth rates. Many economists do not recognize the existence of such waves.

N. D. Kondratiev noted four empirical patterns in the development of large cycles:

Before the beginning of the upward wave of each large cycle, and sometimes at the very beginning of it, significant changes are observed in the conditions of the economic life of society.

Changes are expressed in technical inventions and discoveries, in changing the conditions of money circulation, in strengthening the role of new countries in world economic life, etc. These changes occur constantly to one degree or another, but, according to N. D. Kondratiev, they proceed unevenly and are most intensely expressed before the beginning of the upward waves of large cycles and at their beginning.

The periods of upward waves of large cycles, as a rule, are much richer in major social upheavals and upheavals in the life of society (revolutions, wars) than periods of downward waves.

In order to be convinced of this statement, it is enough to look at the chronology of armed conflicts and upheavals in world history.

The downward waves of these great cycles are accompanied by a prolonged depression in agriculture.

Large cycles of the economic situation are revealed in the same single process of the dynamics of economic development, in which medium cycles with their phases of rise, crisis and depression are also revealed.

Kondratiev's research and conclusions were based on an empirical analysis of a large number of economic indicators of various countries over fairly long periods of time, spanning 100-150 years. These indicators are: price indices, government debt securities, nominal wage, indicators foreign trade turnover, mining of coal, gold, production of lead, iron, etc.

Kondratiev's opponent, D. I. Oparin, pointed out that the time series of the studied economic indicators, although they give larger or smaller deviations from the average value in one direction or another in different periods of economic life, but the nature of these deviations, as for a separate indicator, and by the correlation of indicators, do not allow to single out strict cyclicity. Other opponents pointed to N. D. Kondratiev’s deviations from Marxism, in particular, his use of the “quantity theory of money” to explain the cycles.

Over the past 80 years, the theory of Long Waves by Nikolai Kondratiev has been enriched by the theories of creative destruction by I. Schumpeter, the theory of technical and economic cenoses by L. Badalyan and V. Krivorotov, the theory of technological structures developed by academicians S. Glazyev and Lvov, and the theory of evolutionary cycles by Vladimir Pantin.

The theory of long waves, as well as Nikolai Kondratiev himself, was rehabilitated by the famous Soviet economist S.M. Menshikov in his work “Long waves in the economy. When society changes its skin" (1989).

Dating of the Kondratiev waves

For the period after industrial revolution The following Kondratieff cycles/waves are usually distinguished:

- 1 cycle - from 1803 to 1841-43 (moments of minimums of economic indicators of the world economy are noted)

- 2nd cycle - from 1844-51 to 1890-96

- 3rd cycle - from 1891-96 to 1945-47

- 4 cycle - from 1945-47 to 1981-83

- 5 cycle - from 1981-83 to ~2018 (forecast)

- Cycle 6 - from ~2018 to ~2060 (forecast)

However, there are differences in the dating of the "post-Kondratieff" cycles. Analyzing a number of sources, Grinin L. E. and Korotaev A. V. give the following boundaries for the beginning and end of "post-Kondratieff" waves:

- 3 cycle: 1890-1896 - 1939-1950

- 4 cycle: 1939-1950 - 1984-1991

- 5 cycle: 1984-1991 - ?

Correlation between Kondratieff waves and technological structures

Many researchers associate the change of waves with technological structures. Breakthrough technologies open up opportunities for expanding production and form new sectors of the economy that form a new technological order. In addition, Kondratiev waves are one of the most important forms of implementation of the industrial principles of production.

The summary system of Kondratiev waves and their corresponding technological modes is as follows:

- 1st cycle - textile factories, industrial use coal.

- 2nd cycle - coal mining and ferrous metallurgy, railway construction, steam engine.

- 3rd cycle - heavy engineering, electric power industry, inorganic chemistry, steel production and electric motors.

- 4th cycle - production of cars and other machines, chemical industry, oil refining and internal combustion engines, mass production.

- 5th cycle - development of electronics, robotics, computing, laser and telecommunications technology.

- 6th cycle - possibly NBIC convergence en (convergence of nano-, bio-, information and cognitive technologies).

After the 2030s (2050s according to other sources), a technological singularity is possible, which is not amenable to this moment analysis and forecast. If this hypothesis is correct, then the Kondratiev cycles may end closer to 2030.

Limitations of the Kondratieff Model

Kondratiev waves have not yet received final recognition in world science. Some scientists build calculations, models, forecasts based on K-waves (all over the world and especially in Russia), and a significant part of economists, including the most famous ones, doubt their existence or deny them altogether.

It should be noted that, despite the importance of the cyclical development of society discovered by N. D. Kondratiev for forecasting tasks, his model (as well as any stochastic model) only studies the behavior of the system in a fixed (closed) environment. Such models do not always provide answers to questions related to the nature of the system itself, the behavior of which is being studied. It is well known that the behavior of a system is an important aspect in its study.

However, no less important, and perhaps even the most important, are aspects of the system related to its genesis, structural (gestalt) aspects, aspects of the complementarity of the logic of the system with its subject, etc. It is they that allow us to correctly raise the question of the causes of a particular type of behavior systems depending, for example, on the environment in which it operates.

In this sense, Kondratiev cycles are just a consequence (result) of the system's reaction to the current external environment. The issue of revealing the nature of the process of such a response today and revealing the factors that influence the behavior of systems is relevant. Especially when many, relying on the results of N. D. Kondratiev, A. V. Korotaev and S. P. Kapitsa on the compaction of time, predict a more or less rapid transition of society to a period of permanent crisis.

The concept of the business cycle

In reality, the economy does not develop according to a trend that characterizes economic growth, but cyclically - through constant deviations from the trend, through recessions and ups (Fig. 4.2).

Economic (or business) cycle (business cycle) represents periodic ups and downs in the economy, fluctuations in business activity. These fluctuations irregular and difficult to predict Therefore, the term "cycle" is rather conditional.

Two extreme points of the cycle are distinguished (Fig. 4.2, a): point peak(reak), corresponding to the maximum business activity; point bottom(trough), which corresponds to the minimum of business activity (maximum recession).

Rice. 4.2. The economic cycle and its phases

Phases of the business cycle

The cycle is usually divided into two phases:

decline phase, or recession(recession), which lasts from peak to bottom. A particularly long and deep recession is called depression(depression). It is no coincidence that the crisis of 1929-1933. called the Great Depression;

lifting phase, or revival(recovery), which continues from the bottom to the peak.

There is another approach in which four phases are distinguished in the economic cycle (Fig. 4.2, b), but extreme points are not distinguished, since it is assumed that when the economy reaches a maximum or minimum of business activity, then a certain period of time (sometimes quite long) it is in this state:

I phase - boom(boom), at which the economy reaches its maximum activity. This is the period overemployment(the economy is above potential output, above the trend) and inflation.(Recall that when an economy's actual GDP is higher than its potential GDP, it corresponds to an inflationary gap.) An economy in this state is called "overheated"(overheated economy);

II phase - recession(recession or slump) - business activity begins to decline, actual GDP reaches its potential level and continues to fall below the trend, which leads the economy to the next phase - the crisis;

III phase - a crisis(crisis), or stagnation (stagnation), the economy is in a recessionary gap, because the actual GDP is less than potential. This is a period of underutilization of economic resources, i.e. high unemployment;

IV phase - revival, or recovery, the economy gradually begins to recover from the crisis, the actual GDP approaches its potential level and then exceeds it until it reaches its maximum, which again leads to the boom phase.

Reasons for business cycles

In economic theory, a variety of phenomena were declared to be the causes of economic cycles: the level of solar activity; wars and revolutions; insufficient level of consumption; high population growth rates; optimism and pessimism of investors; change in the money supply; technical and technological innovations; price shocks, etc. The theory political business cycle(political business cycle), proposed by the American economist William Nordhaus, which links the cyclical fluctuations of the economy with the presidential election calendar. If there is a favorable economic situation in the country during the election period (low unemployment and low inflation), it is beneficial for the president at the very beginning of his term in office to destabilize the economy, for example, provoke a recession in order to ensure economic recovery and prosperity by the end of the presidency and be elected for the next term.

In fact, all these reasons can be reduced to one main reason. The main reason for economic cycles - discrepancy between aggregate demand and cumulative supply, between total spending and total output. Therefore, the cyclical nature of the development of the economy can be explained either and change in aggregate demand with a constant aggregate supply (an increase in aggregate spending leads to a rise, their reduction causes a recession); or change in aggregate supply with a constant aggregate demand (a decrease in aggregate supply means a recession in the economy, its growth means a rise).

Behavior of macroeconomic indicators during the cycle

Consider how macroeconomic indicators behave in different phases of the cycle, provided that the cause of the cycle is a change in aggregate demand (aggregate costs).

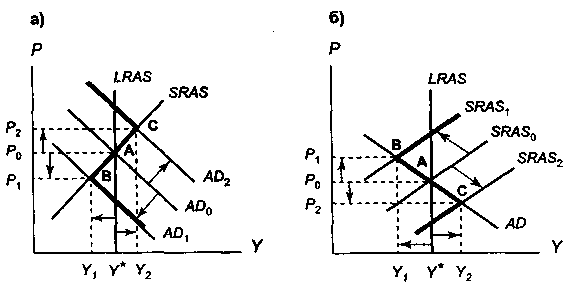

In the boom phase, there comes a moment when the entire amount of output produced cannot be sold, i.e. total spending is less than output. Overstocking occurs, firms are forced to increase stocks of unsold products (inventories), which leads to a curtailment of production and an increase in unemployment, as firms begin to lay off workers. As a result, total incomes fall (household incomes - due to unemployment, firms' incomes - due to the inability to sell part of the output), and, consequently, total expenditures are reduced. Households reduce demand for durable goods. Firms reduce investment demand because it is pointless to expand production in the face of falling aggregate demand. A decrease in total income (taxable base) reduces tax revenues to the state budget. The total amount of state transfer payments is increasing (unemployment benefits, poverty benefits). The state budget deficit is growing. As a result of the fall in aggregate income, imports are decreasing, which may lead to an increase in net exports and a trade surplus. In an attempt to sell their products, firms may begin to reduce their prices, which leads to a decrease in the general price level, i.e. to deflation (in Fig. 4.3, and output is reduced to Y 1, and the price level falls from P 0 to P 1).

Faced with the inability to sell their products even for more low prices, firms (as rationally acting economic agents) can:

or buy more productive equipment and continue production the same kind of goods(if the demand for them is not saturated), but at a lower cost which will reduce product prices without reducing profits, and will also provide an opportunity to increase sales;

or, if the demand for goods produced by the firm is completely saturated and even a price reduction will not lead to an increase in sales, go to production new type of goods which will require technical re-equipment, i.e. replacement of old equipment with a fundamentally new one.

In both cases increasing demand for investment goods. In the industries producing capital goods, a revival begins, employment increases, profits of firms grow. Aggregate incomes are rising, which leads to increased demand and expansion of production in industries producing consumer goods. Recovery, employment growth (decrease in unemployment) and income growth cover the entire economy. The economy is starting to pick up. The price level is rising. Tax revenues are increasing. Transfer payments are declining. The government budget deficit decreases, and a surplus may appear. Income growth leads to an increase in imports, a decrease in net exports and the possible emergence of a balance of payments deficit. The rise in the economy, the growth of business activity turn into a boom, into an "overheating" of the economy ( Y 2 in fig. 4.3, a), after which another decline begins.

The basis of the economic cycle is the change in investment costs. Investment is the most volatile part of aggregate demand (total spending).

Graphically, the cycle can be represented using the model AD- AS (Fig. 4.3). On fig. 4.3, and shows the economic cycle, due to changes in aggregate demand (aggregate costs), and in fig. 4.3, b - changes in the aggregate supply (aggregate output).

In an environment where the downturn in the economy is caused not by a reduction in aggregate demand (aggregate spending), but decrease in aggregate supply most indicators (real GDP, unemployment rate, total income, firms' stocks, sales, firms' profits, tax revenues, transfer payments, etc.) behave similarly. The exception is the general price level, which rises as the recession deepens (Figure 4.3b). This is a situation of stagflation (point B in Fig. 4.3, b) - a simultaneous decline in production (from Y* to Y 1) and an increase in the price level (from R 0 before R 1). Investments also form the basis for getting out of such a recession, as they increase the stock of capital in the economy and create conditions for the growth of aggregate supply (a shift in the curve SRAS 1 right to SRAS 0 ).

Rice. 4.3. Business cycle in the model AD- AS

Business Cycle Indicators

The main indicator of the phases of the cycle is the indicator of the annual GDP growth rate(growth rate - g), which is expressed as a percentage and is calculated by the formula

Thus, this indicator characterizes the percentage change in real GDP (total output) in each subsequent year (Y t ) compared to the previous (Y t - 1), i.e. actually it is not the growth rate, but GDP growth rate. If g - positive value (g > 0), then this means that the economy is in the recovery phase, and if negative (g < 0), then in the decline phase. This indicator is calculated for one year and characterizes the rate economic development- short-term(annual) fluctuations in actual GDP, in contrast to the average annual growth rate ( g a - annual growth rate), which characterizes the rate economic growth, those. long-term upward trend in potential GDP.

Depending on the behavior economic values indicators are distinguished at different phases of the cycle:

procyclical, which increase in the upswing phase and decrease in the downswing phase (real GDP, total income, sales, firms' profits, tax revenues, exchange rates valuable papers, volume of imports);

countercyclical, which increase in the recession phase and decrease in the recovery phase (the unemployment rate, the volume of transfer payments, the value of the inventory of firms, the value of net exports, the state budget deficit, etc.);

acyclic, which are not cyclical in nature, and the value of which is not related to the phases of the cycle (export volume).

In reality, the economy does not develop along a straight line (trend), which characterizes economic growth, but through constant deviations from the trend, through recessions and upswings. The economy develops cyclically (Fig. 1.). The economic (or business) cycle (business cycle) is a periodic ups and downs in the economy, fluctuations in business activity. These fluctuations are irregular and unpredictable, so the term "cycle" is rather arbitrary. There are two extreme points of the cycle: 1) the peak point (peak), corresponding to the maximum business activity; 2) the bottom point (trough), which corresponds to the minimum business activity (maximum decline).

The cycle is usually divided into two phases (Fig. 1. (a)): 1) a recession phase or recession (recession), which lasts from peak to bottom. A particularly long and deep recession is called a depression. It is no coincidence that the crisis of 1929-1933 was called the Great Depression; 2) the phase of recovery or recovery (recovery), which continues from the bottom to the peak.

There is another approach in which four phases are distinguished in the economic cycle (Fig. 1.(b)), but extreme points are not distinguished, since it is assumed that when the economy reaches a maximum or minimum of business activity, then a certain period of time (sometimes enough long) it is in this state: 1) Phase I - boom (boom), in which the economy reaches its maximum activity. This is a period of overemployment (the economy is above the level of potential output, above the trend) and inflation. (Recall that when actual GDP is higher than potential GDP in an economy, this corresponds to an inflationary gap.) An economy in this state is called an "overheated economy"; 2) P phase - recession (recession or slump). The economy gradually returns to the level of the trend (potential GDP), the level of business activity is reduced, the actual GDP reaches its potential level, and then begins to fall below the trend, which leads the economy to the next phase - the crisis; 3) III phase - crisis (crisis) or stagnation (stagnation). The economy is in a recessionary gap because actual GDP is less than potential. This is a period of underutilization of economic resources, i.e. high unemployment; 4) Phase IV - recovery or recovery. The economy gradually begins to recover from the crisis, the actual GDP approaches its potential level, and then exceeds it until it reaches its maximum, which again leads to the boom phase.

Causes of the business cycle

In economic theory, a variety of phenomena were declared to be the causes of economic cycles: spots on the sun and the level of solar activity; wars, revolutions and military coups; presidential elections; insufficient level of consumption; high population growth rates; optimism and pessimism of investors; change in the money supply; technical and technological innovations; price shocks and others. In fact, all these reasons can be reduced to one. The main reason for economic cycles is the discrepancy between aggregate demand and aggregate supply, between aggregate spending and aggregate production. Therefore, the cyclical nature of the development of the economy can be explained: either by a change in aggregate demand with a constant value of aggregate supply (an increase in aggregate spending leads to an increase, their reduction causes a recession); or a change in aggregate supply with a constant value of aggregate demand (a decrease in aggregate supply means a recession in the economy, its growth means a rise).

Let's consider how indicators behave at different phases of the cycle, provided that the cause of the cycle is a change in aggregate demand (aggregate costs) (Fig. 2. (a)).

In the boom phase, there comes a moment when the entire volume of production produced cannot be sold, i.e. total spending is less than output. Overstocking occurs, and firms are initially forced to increase inventory. The growth of stocks leads to curtailment of production. The reduction in production leads to the fact that firms lay off workers, i.e. the unemployment rate is rising. As a result, aggregate incomes fall (consumer income due to unemployment, investment income due to the senselessness of expanding production in the face of a fall in aggregate demand), and, consequently, aggregate spending. Households, first of all, reduce the demand for durable goods. Due to the falling demand of firms for investment and household demand for durable goods, the short-term interest rate (the price of investment and consumer credit) is falling.

The long-term interest rate tends to rise (in a context of declining incomes and a shortage of cash, people start selling bonds, the supply of bonds increases, their price falls, and the lower the price of a bond, the higher the interest rate). Due to the decrease in total revenues (taxable base), tax revenues to the state budget are reduced. The amount of state transfer payments is increasing (unemployment benefits, poverty benefits). The state budget deficit is growing. In an attempt to sell their products, firms can reduce their prices, which can lead to a decrease in the general price level, i.e. to deflation (in Fig. 2. (a) output is reduced to Y1, and the price level falls from P0 to P1).

Faced with the inability to sell their products even at lower prices, firms (as rational economic agents) can either buy more productive equipment and continue to produce the same type of goods, but at a lower cost, which will reduce product prices without reducing profit margins. (it is advisable to do this if the demand for goods produced by firms is not saturated, and a price decrease in conditions low income will provide an opportunity to increase sales volume); or (if the demand for goods produced by the company is fully saturated and even a price reduction will not lead to an increase in sales) switch to the production of a new type of goods, which will require technical re-equipment, i.e. replacement of old equipment with fundamentally new equipment. In both cases, the demand for capital goods increases, which serves as an incentive for the expansion of production in industries producing capital goods. A revival begins there, employment increases, profits of firms grow, aggregate incomes increase. Income growth leads to an increase in demand in industries producing consumer goods, and to the expansion of production there. Recovery, employment growth (decrease in unemployment) and income growth cover the entire economy. The economy is starting to pick up. The growth in demand for investments and for durable goods leads to an increase in the cost of credit, i.e. an increase in the short-term interest rate. The long-term interest rate decreases as the demand for bonds increases and, as a result, the prices (market rate) of securities rise. The price level is rising. Tax revenues are increasing. Transfer payments are declining. The government budget deficit decreases, and a surplus may appear. The rise in the economy, the growth of business activity turn into a boom, into an “overheating” of the economy (Y2 in Fig. 2.(a)), after which another recession begins. So, the basis of the economic cycle is the change in investment spending. Investment is the most volatile part of aggregate demand (total spending).

On fig. 2. The cycle is represented graphically using the AD-AS model. On fig. 2.(a) shows the business cycle driven by changes in aggregate demand (aggregate spending), and fig. 2.(b) - changes in the aggregate supply (aggregate output).

In conditions when the recession in the economy is caused not by a reduction in aggregate demand (aggregate spending), but by a decrease in aggregate supply, most indicators behave in the same way as in the first case (real GDP, unemployment rate, aggregate income, firms' stocks, sales , profits of firms, tax revenues, the volume of transfer payments, etc.) The exception is the indicator of the general price level, which rises as the recession deepens (Fig. 2. (b)). This is a situation of "stagflation" - a simultaneous decline in production (from Y * to Y1) and an increase in the price level (from P0 to P1). Investments also form the basis for getting out of such a recession, as they increase the stock of capital in the economy and create conditions for the growth of aggregate supply (shift of the SRAS1 curve to the right to SRAS0).

Business Cycle Indicators

The main indicator of the phases of the cycle is the indicator of the rate of economic growth (rate of growth - g), which is expressed as a percentage and calculated by the formula: g = [(Yt - Yt - 1) / Yt - 1 ] x 100%, where Yt is real GDP current year, and Yt – 1 is the real GDP of the previous year. Thus, this indicator characterizes the percentage change in real GDP (total output) in each next year compared to the previous one, i.e. actually not the growth rate (growth), but the rate of GDP growth. If this value is positive, then this means that the economy is in a phase of growth, and if it is negative, then it means that it is in a phase of recession. This indicator is calculated for one year and characterizes the rate of economic development, i.e. short-term (annual) fluctuations in actual GDP, in contrast to the average annual growth rate used in calculating the rate of economic growth, i.e. long-term upward trend in potential GDP.

Depending on the behavior of economic values at different phases of the cycle, indicators are distinguished:

- procyclical, which increase in the upswing phase and decrease in the downswing phase (real GDP, total income, sales, firms' profits, tax revenues, transfer payments, imports);

- countercyclical, which increase in the recession phase and decrease in the recovery phase (unemployment rate, stocks of firms);

- acyclic, which are not cyclical in nature and the value of which is not related to the phases of the cycle (export volume, tax rate, depreciation rate).

Types of cycles

There are different types of cycles by duration:

- centennial cycles lasting a hundred or more years;

- "Kondratiev cycles", the duration of which is 50-70 years and which are named after the outstanding Russian economist N.D. Kondratiev, who developed the theory of "long waves of the economic situation" (Kondratiev suggested that the most destructive crises occur when the points of maximum fall coincide business activity of the "long-wave cycle" and the classical; examples are the crisis of 1873, the Great Depression of 1929-1933, the stagflation of 1974-1975);

- classical cycles (the first "classical" crisis (crisis of overproduction) occurred in England in 1825, and starting from 1856 such crises became global), which last 10-12 years and are associated with a massive renewal of fixed capital, i.e. equipment (due to the increasing value of the obsolescence of fixed capital, the duration of such cycles has decreased in modern conditions);

- Kitchin cycles lasting 2-3 years.

The allocation of different types of economic cycles is based on the duration of operation various kinds physical capital in the economy. Thus, centennial cycles are associated with the emergence of scientific discoveries and inventions that make a real revolution in production technology (remember, the “age of steam” was replaced by the “age of electricity”, and then the “age of electronics and automation”). Long-wavelength Kondratiev cycles are based on the service life of industrial and non-industrial buildings and structures (the passive part of physical capital). Approximately after 10-12 years, the equipment (the active part of physical capital) wears out, which explains the duration of the “classic” cycles. In modern conditions, of paramount importance for the replacement of equipment is not physical, but its moral depreciation, which occurs in connection with the appearance of more productive, more advanced equipment, and since fundamentally new technical and technological solutions appear with a frequency of 4-6 years, then the duration of the cycles becomes shorter. In addition, many economists attribute the duration of cycles to the massive renewal of consumer durables (some economists even suggest that they be classified as investment goods purchased by households) occurring at intervals of 2-3 years.

IN modern economy the duration of the phases of the cycle and the amplitude of the oscillations can be very different. It depends, first of all, on the cause of the crisis, as well as on the characteristics of the economy in different countries: the degree of state intervention, the nature of economic regulation, the share and level of development of the service sector (non-productive sector), the conditions for the development and use of the scientific and technological revolution.

Cyclic fluctuations are important to distinguish from non-cyclical fluctuations. The business cycle is characterized by the fact that all indicators change, and that the cycle covers all industries (or sectors). Non-cyclic fluctuations are reflected:

- a change in business activity only in some sectors that have a seasonal nature of work (an increase in business activity, for example, in agriculture in the fall during the harvest season and in construction in spring and summer, and a decline in business activity in these sectors in winter);

- in changing only some economic indicators (for example, a sharp increase in the volume retail sales before the holidays and the growth of business activity in the respective industries).

Economic processes are a delicate balance between supply and demand, aggregate production and sales. The more stable this balance, the more harmoniously the development of the national economy takes place, and the well-being of the population grows.

But in the economy of a country with a market system of trade relations, there are fluctuations. They are cyclically repeated. Such movement determines the phases of the economic cycle. Any trend in the development of the national economy goes through these stages. Given such a movement, it is possible to more accurately predict the financial and economic state of the state in different periods of time and adjust Negative consequences possible jumps.

cyclicality

The phases of the economic cycle exist due to the uneven processes in the national economy. Ups are followed by downs and vice versa. The sequence of phases of economic development is characterized by cyclicality. Since 1825, each country has been moving according to this scenario. It was in this year that the first financial and economic large-scale crisis erupted.

Production first expands and then freezes. Sometimes the downturn in business activity is simply colossal. Growth is replaced by a recession phase of the economic cycle. This is typical for any movement in the trend of the welfare of the country's economy. This movement is called cyclical. It has a characteristic. The movement of the cyclic function is in a spiral, not in a circle. Therefore, the general trend leads to an increase in the welfare of society.

What is a business cycle?

The theory of economic cycles investigates the behavior of the system at various points on the curve of development of the national economy. This allows you to establish the causes of fluctuations and predict them in the future.

The economic cycle is the main object of the theory of the development of national economic activity. It represents fluctuations in activity indicators. These include GNP, total sales, price level, unemployment, investment, capacity utilization.

In one cycle, the trend development curve goes through certain stages. These are the phases. Their economic cycle has 4 main points: boom, recession, crisis, recovery. Cyclicity contributes to the regulation of the processes of the system and their compliance with the changing conditions of the economy. All fluctuations are different. But cycles have a lot in common.

Reasons for fluctuations

The theory of economic cycles studies the causes that can cause fluctuations in the system. There are many factors that can upset the balance. These include natural fluctuations, wars, revolutions, elections, lack of consumption, and population growth. The mood of investors, the presence of technological innovations and innovations are also important.

All existing reasons can be reduced to one. This is the mismatch between aggregate demand and supply. One factor is subject to change, and the second remains unchanged. Because of this, phases of the cycle arise, which are characterized by certain qualities.

Decline phase

One of the phases of the cycle is the financial and economic crisis. It is also called compression, recession. The crisis has certain features. Initially consumption drops. At the same time, supply is growing, stocks are accumulating. To sell them faster, the company is forced to reduce the price. Then production volumes fall. Many companies go bankrupt or collapse. The reduction in production leads to unemployment and lower incomes of the population. The standard of living is deteriorating. Ordinary people and organizations start looking for sources of additional funding. Therefore, the credit rate, the payment for the use of borrowed capital is growing.

The crisis of 1929-1933 is recognized as the most famous recession of the economic cycle. It covered many countries, led to a real decrease in the income of the population by 58%.

Depression

The apogee of the crisis is observed in the phase of reaching the bottom - the lowest point of the recession production activity. It is also called depression.

The recession phase of the business cycle ends. There is a turning point. The price level stabilizes, the reduction in production stops. The stocks of companies are bouncing back, and the lending process is also stabilizing. Business activity at this point is so low that even the demand for borrowed capital falls.

At the bottom of the cycle, there is the highest level of unemployment. The stabilization of prices contributes to the way out of the crisis. The growth process starts from this point.

Recovery phase

The growth of the economy is in the recovery phase. There is a gradual increase in production. The business activity of enterprises is increasing, people are getting more salaries, new jobs are opening up.

The purchasing power of the population is increasing. This leads to higher prices. To meet the increasing demand, companies are purchasing new equipment. As a result, the need for money increases. The interest rate goes up again.

In this period, the economy is inexorably approaching the pre-crisis level of development. Since cyclicity is a process of development, the growth phase soon brings the national economy to the line it reached in the last cycle. And the final stage begins.

boom phase

The boom phase of the business cycle drives the system up. It reaches the pre-crisis level of development and exceeds it. This stage is called expansion, expansion, boom. During this time, unemployment is at its lowest. There is an increase in the income of the population. According to the purchasing power of the enterprise set the highest prices for their products. Production is carried out to the limit of its capabilities. Demand exceeds supply.

This continues to the very top of the cycle. In it, the price is set at such a high level that consumption begins to decline. Sales problems reappear. This is the beginning of a new phase of the economic cycle. He is entering a recession.

All these processes contribute to the emergence of cyclicity. However, the regularity of such fluctuations is typical only for a market economy. With a mixed control system economic activity sequence is broken. Some features of the phases have also undergone changes.

Varieties of cycles

The sequence of phases of the economic cycle is most often the same. But the duration of the period itself, during which there is a complete change of points on the business activity curve, is different. There are centennial, classical, short and long cycles.

In the first case, the phases replace each other with a duration of more than a century. Long cycles are 50-70 years. Classic varieties last 10-12 years. If long and medium cycle downturns coincide, the most destructive processes for the economy occur.

Average fluctuations are associated with the massive renewal of non-circulating capital. The shortest cycles are only 2-3 years long.

The allocation of different types of fluctuation lengths is associated with the use of various types of capital in the economy. The duration of the phases is very different. It depends on the causes of the crisis, as well as on the characteristics of the country.

One should also distinguish between cyclic and non-cyclic oscillations. In the first case, all indicators in existing industries change. Non-cyclical fluctuations affect only some industries and economic indicators. Their nature is local and is associated with other reasons that do not affect the overall business activity (for example, seasonal goods, increased demand before the holidays, etc.).

Having studied the phases of the economic cycle, it is possible to make more adequate forecasting in the field of fluctuations in business activity. This makes it possible to reduce the destructive nature of the crisis and raise the line of production growth.