Every entrepreneur thinks about earning methods and ways to make a profit. In any production there are costs - the costs of manufacturing and selling goods. They will be deducted from the received revenue, the result of the calculations will be profit (positive value) or loss (negative value).

For profitable operation, the management of the enterprise must know the boundary value of the transition of loss into profit. This is called the breakeven point. It is used by investors to determine the probability and payback period of projects.

The break-even point can be determined using mathematical calculations or graphically. The value will be in monetary or natural terms.

What

The break-even point or critical volume is considered to be the amount of production at which the income received from sales will cover the total costs. In other words, this is the size of the minimum profit in monetary terms or the quantity of products sold, which compensates for the costs.

Work at this point indicates the absence of profit and costs at the same time. With an increase in volume by at least 1 unit, the enterprise will begin to work in profit. The break-even point is often referred to as the profitability threshold.

Purpose

The break-even point value is used to analyze the current financial condition and allows you to plan ahead. The indicator allows you to:

- evaluate financial stability and solvency, which is used by investors, management and creditors;

- calculate the feasibility of expanding and mastering new types of products, technologies;

- see the dynamics of the indicator, identify bottlenecks in production;

- sales plan planning;

- establish an acceptable reduction in revenue, which will allow you to remain in profit;

- trace the impact of production costs, the cost of goods and the volume sold on the financial result.

Calculation

The calculation can be made different ways depending on the type of costs. Consider the classical order that underlies the rest of the methods.

Data for calculation

To correctly determine the value of the break-even point, it is necessary to distinguish between constants and variable costs and know:

- unit cost of goods R;

- produced and sold volume - Q;

- proceeds received - AT(not required to determine the threshold of profitability);

- the amount of fixed costs - Zpost.

- variable costs - Zper.

Fixed costs are costs incurred that do not depend on the volume produced, that is, they remain unchanged for a long time. These include:

- wages with insurance premiums for managerial and engineering staff;

- rental of premises;

- tax payments;

- depreciation;

- leasing obligations.

Variable costs are costs that depend on the quantity of output produced. They have different meanings and respond quickly to changes in production. Variable costs are:

- the price of raw materials, spare parts and components;

- piecework wages and insurance payments for production workers;

- HMS, electricity, fuel;

- transportation.

The division of costs is conditional and is used to determine the break-even point. The specificity of some enterprises implies a more detailed division according to economic meaning. For example, production costs are:

- conditionally permanent: storage and warehouse movement of components;

- conditional variables: the cost of current and scheduled repairs.

There are several cost accounting systems: variable costing, direct costing, standard costing, etc. Each type of cost can be individual for a certain type of product.

Formula

The mathematical method (VER) allows you to determine the break-even points in natural and monetary terms. The classical scheme involves the calculation for one product. If it is necessary to determine the indicator for several types of products, then averaged data are used in the calculation. The following assumptions apply:

- Each type of cost and the cost of the goods remain constant for the selected volume.

- Directly proportional change in output and cost.

- Production capacity in the period chosen for the calculation are constant.

- Unchanged product range.

- Insignificant influence of stocks - the share of work in progress is small, and all products are sold for sale.

BEP is often confused with the payback period of a project. This is the time after which the organization will receive a return on investment.

Definition in monetary terms

Using the calculation, you can find out the minimum value of revenue, which will help cover the costs of production and sales. Profit will be 0.

VERDEN \u003d V * Zpost / MD

MD = V-Zper

B \u003d P * Q

AT- revenue;

P- the cost of production;

Q- produced volume;

MD- marginal income, which can be calculated per unit of production, taking into account the fact that revenue will be equal to the product of price and volume.

MD for 1 unit. \u003d P - Zper. for 1 unit

The break-even point in monetary terms is found through the marginal income ratio - Kmd:

Kdm \u003d MD / V \u003d MD for 1 unit / R

VERDEN = Zpost/Kmd

The final value when calculating according to the two formulas must match.

Definition in kind

The above formula allows you to determine the minimum volume of sold products that can cover production costs and lead to zero profit.

VERNAT \u003d Zpost / (P-Zper by 1 unit)

Each subsequent unit that allows you to exceed a certain volume will bring profit to the organization. If the break-even point is known in physical terms, then it is easy to calculate the break-even point in monetary terms:

VERDEN \u003d VERNat * P

Graphic method

The graphical method allows you to determine the break-even point without mathematical calculations. Build a graph that indicates revenue, fixed and variable costs. The horizontal axis will be the volume, and the vertical axis will be the amount of costs and revenues in rubles.

The break-even point will be at the intersection of total costs and revenue. On the graph, this value is equal to 91.67 pieces with a revenue of 22,916.67 rubles.

Calculation in Excel

For the convenience of the calculation, you can use the Excel office application. It is easy to establish a connection between data and build tables with graphs for comparison.

Compiling a table

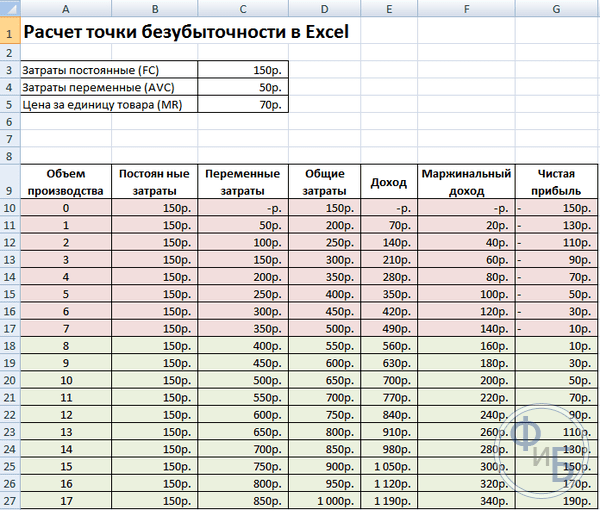

It is necessary to start calculating the break-even point by entering data on costs and the cost of goods. For example, fixed costs are 150 rubles, variable costs are 50 rubles, and the cost of a unit of goods is 70 rubles.

Based on the entered data and production volume, a table is formed, where the dynamics of changes in net profit or loss should be traced. This is necessary to determine the break-even point.

Let's create a second table with columns:

- Volume of production.

- Fixed costs.

- variable costs.

- General costs.

- Revenue.

- Marginal income.

- Net profit.

The volume of production is chosen independently. In the example, 0-20 pieces are taken. Fixed costs are transferred from the first table of cell D3. Since fixed costs do not depend on the volume of products produced, their value remains unchanged throughout the column. To preserve the value of a cell when propagating values, the address is preceded by a $ sign - $D$3.

Variable costs are determined by the formula:

Zper = Q*Zper per 1 unit. = A9*$D$4

Total costs, they are also called gross, are equal to the sum of variable and fixed costs - B9 + C9.

Revenue or income is equal to the product of volume and the cost of a unit of goods - A9*$D$5, and marginal income - E9-C9.

Net profit, as mentioned above, is equal to marginal income minus fixed costs: E9-C9-B9.

From the eighth unit, the organization will begin to make a profit. With a smaller volume, revenue cannot cover the total costs. The first profit is 10 rubles, that is, this is not quite a break-even point, when total costs are equal to revenue. The exact value can be determined by the formula:

TBnat \u003d 150 / (70-50) \u003d 7.5 pcs.

The mathematical value of the break-even point is 7.5, but it is not possible to produce some part of the whole product. Economists round up the value - 8 pcs. The proceeds will be 560 rubles.

Two additional indicators can be added to the table - the margin of safety (margin of safety) in monetary and percentage terms (KB%, KBden). This will help determine how much revenue is missing before the break-even point is reached, and how much total cost reductions need to be made to reach the break-even point at a given volume. By these coefficients, you can determine a safe financial position - when it reaches 30%.

KBden = Vfact - Wtb = E9-$E$14

KB% \u003d KBden * 100% / Vfact \u003d H10 / E10 * 100

Wtb- revenue for the security point;

In fact- actual income.

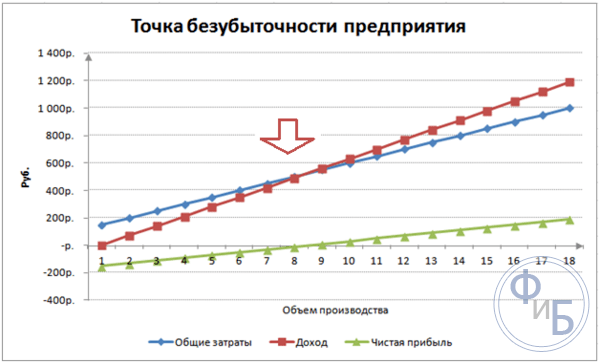

Plotting

For understanding, build a graph. There are several types of charts in Excel. The best perception of information in this example will be a scatter plot, which is located in the "Insert" tab. The horizontal axis shows the volume of products produced, and the vertical axis - revenue and the amount of costs. Data to build:

- total costs;

- net profit;

- revenue.

There are three straight lines on the graph. The intersection of total costs and revenue will be at the break-even point. It shows net profit of zero horizontally and the minimum revenue to cover the costs incurred vertically.

To build a detailed graph with marginal income and variable costs, you need to expand the amount of data.

Calculation example

The simplest are the calculations for mono production, when the organization produces the same type of product. Multi-product tasks have their own characteristics, which should be taken into account when calculating the break-even point.

One item

Consider a common example of entrepreneurial earnings - trading in the market. The commodity is watermelons with a fixed value throughout the city. Watermelons are bought in the southern regions and brought to the central part of the country. The business is seasonal, but quite profitable.

Basic indicators:

- the cost of 1 watermelon is 250 rubles;

- Zper for 1 unit. (seller's salary, wholesale purchase) - 130 rubles;

- Zpost (taxes, rent of a place in the market, transportation, packaging) - 11,000 rubles. per month;

- monthly revenue - 36,000 rubles.

For successful planning, it is required to calculate the minimum sales volume and the profit value to cover the costs incurred.

The indicated cost is an average, since the weight of each watermelon is different. These values can be neglected in the calculation.

Determination of the break-even point:

VERNAT \u003d 11000 / (250-130) \u003d 92 pcs.

To determine in monetary terms, calculate the volume of watermelons sold and the value of variable costs for this volume:

Q month = 36000/250 = 144 pcs;

Zper per volume \u003d 130 * 144 \u003d 18720 rubles.

Let's determine the profitability threshold in money according to various formulas:

VERDEN \u003d 3600 * 11000 / (36000-18720) \u003d 22916.67 rubles

VER den \u003d Zpost / ((250-130) / 250) \u003d 22916.67 rubles

VERDEN \u003d 92 * 250 \u003d 23,000 rubles

The first and second values show the break-even point when the profit is 0. At the same time, the sales volume is 91.67 watermelons, which is incorrect information. The third indicator is based on the critical volume of 92 watermelons.

The comparison shows that the monthly revenue exceeds the break-even point, which allows us to talk about profit.

Safety Edge:

KBden \u003d 36000-23000 \u003d 13000 rubles;

KB% = 13000/36000 * 100% = 36.11%

The level is more than 30%, which indicates the correctness of business planning.

Multi-product task

Consider the settlement procedure for a store that sells four goods: A, B, C and D. The store incurs fixed costs and has variable costs for each type separately. The purchase is made from different suppliers, the proceeds from the sale are also different.

Initial data:

- A: revenue 370 thousand rubles, variable costs 160 thousand rubles;

- B: revenue 310 thousand rubles, variable costs 140 thousand rubles;

- B: revenue 340 thousand rubles, variable costs 115 thousand rubles;

- G: revenue 70 thousand rubles, variable costs 40 thousand rubles.

The amount of total revenue is 990 thousand rubles, and variable costs are 455 thousand rubles.

The revenue structure remains constant. Due to the fact that the range and cost of goods is different, it is better to calculate the break-even point in monetary terms. The solution will be based on the direct costing method, which assumes a range of values:

VERDEN \u003d Zpost / (1-Kz.per.);

Short lane. - share of variable costs in revenue:

Kz.per. = Zper/V

- A - 0.43;

- B - 0.45;

- B - 0.48;

- G - 0.57;

- General short circuit - 0.46.

Let's define marginal income and its share in revenue:

- A - 210 thousand rubles, 0.37;

- B - 170 thousand rubles, 0.55;

- B - 125 thousand rubles, 0.52;

- G - 30 thousand rubles, 0.43;

- The total value is 535 thousand rubles, 0.54.

Let's calculate the average break-even point:

VERDEN Wed = 400 / (1-0.46) = 740.74 thousand rubles.

Next, consider the most optimistic forecast - marginal ordering in descending order. The first two products A and B will have the highest profitability. Initially, the store should sell these products, which will provide a marginal income of 210 + 170 = 380 thousand rubles. This will almost cover fixed costs of 400 thousand rubles. The rest can be taken from the third item. The break-even point will be reached after the sale of the following goods:

VERDEN. opt. \u003d 370 + 310 + (20 * 240/125) \u003d 718.4 thousand rubles.

The pessimistic forecast or marginal order in ascending order will be the sale of G, C, B. The total marginal income is 325 thousand rubles, which will not allow covering fixed costs. The remaining 75 thousand rubles must be received from the sale of product A. The value of the break-even point:

VERDEN. pessimistic \u003d 70 + 240 + 310 + (75 * 370 / 210) \u003d 752.14 thousand rubles.

As you can see, the value of the break-even point in the three cases is different. Optimistic and pessimistic values give an interval of possible break-even points.

Let's define the edge of safety in percent and rubles:

KBden \u003d 990-740.74 \u003d 249.26 thousand rubles;

KB% = 249.26/990*100% = 25.18%.

Despite the presence of profit, the safety margin of the store is less than 30%. It is necessary to take measures to improve the financial performance. To do this, it will be necessary to reduce Zper and increase the volumes for goods A, C and D. It will not be superfluous to check fixed costs in detail in order to find reserves for their reduction.

Calculation for the enterprise

Consider an organization that produces household solvent, which is sold in liter containers. The company is small, the cost rarely changes, which allows you to calculate the break-even point in physical terms.

Data for calculation:

- the cost of one bottle is 140 rubles;

- variable costs for 1 liter - 80 rubles;

- fixed costs - 170 thousand rubles;

- revenue - 450 thousand rubles;

- volume - 3 thousand rubles.

VERNAT. \u003d 170,000 / (140-80) \u003d 2833.33 pcs.

The calculated value is close to the actual volume - 3000 pcs.

Let's define the edge of safety:

KBnat. = 3000 - 2834 = 166 pcs.

KB% = 166/3000 * 100% = 5.53%

It can be concluded that the company is on the verge of breakeven. Urgent measures should be taken to improve the situation: the cost structure should be reviewed, the salaries of management personnel are likely to be overstated. Work out variable costs in detail and find cheaper suppliers.

Advantages and disadvantages of calculations

The main advantage of calculating the break-even point allows you to quickly and easily analyze the level of production or sales that is necessary to achieve a minimum critical level. The disadvantage of the above model is the construction restrictions:

- Linear change in sales and production. This does not allow us to take into account the sharp surges and changes that occur in reality. Linearity does not take into account seasonality, a decrease or increase in demand, or the entry of new competitors into the market. All this affects future demand, and, accordingly, sales volumes. New technologies can be introduced into production, which increases production volumes.

- The model has high efficiency in a low-competitive market with stable consumer demand for manufactured products. Globalization is becoming the culprit of market stability.

- Sales volume depends on many factors: marketing, dealer network size, product quality, seasonality, etc.

- Such calculations do not show an adequate picture for small enterprises in which the nature of sales is unstable.

Break even planning

The listed methods are easy to calculate for one product and are suitable for companies with a stable market and a constant selling price.

However, there are a number of disadvantages:

- it is impossible to take into account seasonality and cost fluctuations;

- markets often become more specific, progressive technologies and marketing moves appear;

- the cost of raw materials may vary;

- discounts are provided to regular customers and wholesalers, which is not taken into account in the formula.

The analysis of the break-even point should take place in conjunction with various factors and economic indicators.

According to the data obtained, the current market conjecture and significant factors affecting the cost are analyzed. Planning consists in forecasting costs and competitive costs. The data is needed for the break-even plan and the size of production, which are entered into financial plan organizations. For effective functioning, it is periodically necessary to monitor the implementation of the approved goals.

Planning stages:

- Analysis of the current situation. It is necessary to identify weak and strengths, as well as ways to reduce costs, taking into account external and internal factors. An assessment is given to sales and marketing services, the level of rationality production process and management. Among the external factors, they necessarily consider the occupied market share, the work of competitors, controlled companies, the economic and political situation, and changes in consumer demand.

- Forecasting the value in the future, taking into account the factors discussed earlier. There is a study of alternative sales options, a competitive margin range is planned, the possibility of restructuring to the production of similar products in the event of an unfavorable situation is being considered.

- Calculation of cost, fixed and variable costs. The size of work in progress, the need for working capital and fixed assets, sources of acquisition are determined working capital. The costs should take into account the possible costs of leasing, credit and similar obligations.

- Calculation of the break-even point. The required size of the safety edge is calculated: the less stable the external environment, the larger the safety edge should be. Then the output volume is determined taking into account the safety edge.

- Cost planning. The price of a product that will help achieve the desired level of sales is calculated. With the new cost, the break-even point, the margin of safety, is re-determined. If necessary, then steps 3 and 4 are repeated to search for reserves to reduce the cost and achieve the required margin of safety.

- Approval of the final sales plan and break-even by periods. Approval is made according to the value of the critical volume.

- Breakeven control. It takes place in several stages: control of expense items, sales plan, cost, transfer of payment from buyers. The management of the organization should always know the level of compliance of the current position with the planned break-even value.

The break-even point calculation helps determine the minimum production or sales frontier for organizations. The model is well used on large-scale production with a stable market. The break-even point model allows you to find a safe zone - the company's distance from the critical value, when profit becomes zero.

As you know, every company carries out its activities for profit. Only when this goal is achieved can the firm ensure the stability of its work and the basis for expansion. The profit of the enterprise is expressed in the form of dividends on invested funds. The profitability of the company attracts investors, helps to increase its capital. One of the most important aspects of the activity is the concept of break-even. It is considered the first step towards obtaining accounting, and then economic profit. Let's take a look at what a financial break-even point is.

Theoretical aspect

In economic science, the definition of the break-even point is understood as the normal state of the company in today's competitive market, which is characterized by long-term equilibrium. At the same time, economic revenue is taken into account - income at which the company's costs include the average market rate of return on invested funds. Normal income of the company is also taken into account. Under these assumptions, the definition of the break-even point is as follows:

- This is the volume of sales of a product, in which the profit from the sale fully covers the costs of its release, including the average market interest on own assets and entrepreneurial (normal) income.

Operational efficiency

If the company earns an accounting profit (the balance of its sales revenues and cash costs for the release of goods is positive), the break-even point may not be reached economically. For example, revenue may be below the average market interest on capital. It follows from this that there are other, more profitable options use of own assets, which would allow to receive more income. The break-even point of the enterprise, thus, acts as a criterion for evaluating the effectiveness entrepreneurial activity. A company that does not achieve it is operating ineffectively in the current market conditions. But this fact, of course, cannot be considered an unequivocal reason for the company to go out of business. To resolve the issue of termination of the company's activities, it is necessary to study the cost structure in detail.

Revenue maximization

It is necessary for the optimal functioning of the company. The maximization process is the calculation of the break-even point in economic terms. In the study of this procedure, the following concepts are used:

- marginal income. It represents the amount by which the total profit of the company changes when the output of a product increases by 1 unit.

- marginal cost. They express the amount by which total costs change when output increases by 1.

- Total average cost is the sum of fixed, variable and sunk costs per unit of output.

From a certain moment (when a certain volume of output is established), the variable cost curve will be increasing, and marginal revenue, respectively, decreasing. For profit maximization, the ratio between profit and costs with an increase in output by 1 is fundamental. It is clear that when marginal cost is less than income, profit becomes larger with an increase in the quantity of goods. If costs are greater than revenue, then a decrease in output will increase revenue. Thus, it is possible to formulate a criterion under which the profit will be maximum: it is achieved when the marginal indicators of revenue and costs are equal.

Break-even point: how to calculate?

There are several points to be noted Special attention. First of all, the problem is to establish the critical volume of goods at which the break-even point of production is reached. There are three approaches to solving this problem:

- The equation.

- Establishment of marginal income.

- Graphic image.

Also of particular importance will be the analysis of the break-even point (predictive setting) to changes in assumptions.

The equation

This break-even point method involves drawing up the following scheme:

- Income - Variable costs - Fixed costs = Net profit.

The latter indicator can be denoted as P. P - the selling price of a unit of goods produced, x - the volume of manufactured and sold products for the period, a - fixed and v - variable costs. Using these notations, we can write the following equation:

- P \u003d P * x - (a + b * x), or P \u003d (P - c) * x - a.

The last equality indicates that all factors are divided into criteria that depend and do not depend on the volume of implementation. In the process of determining the parameters, the costs were divided into sold and manufactured products. This difference is considered the most significant in two approaches to management accounting: Direct costing and Absorption costing. In the latter case, costing is performed with the distribution of all costs between sold goods and its remainder. In other words, fixed costs are resource intensive. When using the second method, fixed costs are attributed entirely to implementation. According to the first equation, you can easily calculate the break-even point. For this, simple mathematical transformations should be carried out. From the condition P = 0, the volume of output of goods is established, at which the break-even point is reached in the company. The formula looks like this:

- ho \u003d (P + a): (P - c) \u003d a: (P - c).

Example

Consider a hypothetical company producing electronic components. The cost of one unit of goods is $5,000, variable costs (the price of components, staff salaries, and so on) for 1 product are $4,000, fixed costs are $20,000. Let's find the maximum production volume at which the the firm's break-even point. The formula will be:

- xo \u003d 20,000: (5000 - 4000) \u003d 20 (units of production).

The time for which the found quantity must be released and sold will correspond to the period for which the value of fixed costs will be found. Using the equation in the previous paragraph, you can determine the amount of output that must be achieved to obtain a specific amount of profit, which will reach the break-even point. How to calculate the company's income, for example, in 10 thousand dollars? To do this, you need to issue:

- x \u003d (10,000 + 20,000): (5000 - 4000) \u003d 30 (units).

Marginal profit

This method is considered a modified version of the previous method. Marginal profit will be considered the income that the company will receive from the release of one product. Using the example, let's find it:

5000 - 4000 = 1000 per item.

For a more accurate representation of the area of relevance, it is necessary to list the assumptions that are used in the construction of the described models.

General expenses and revenue

The behavior of these indicators is linear within the scope of relevance and is rigidly defined. This provision is true only when the change in output is small in comparison with the market capacity. this product. Otherwise, the linearity of the relationship between output and revenue indicators will be violated.

Expenses

All costs can be divided into fixed and variable. The former are independent of the volume of output within the scope of relevance. This assumption greatly simplifies the analysis. However, at the same time, it significantly limits the scope of relevance. Indeed, under this assumption, the volume is limited by the available fixed assets. However, it is not possible to increase them or rent them. A more realistic assumption is that the change in fixed costs occurs in steps. But it greatly complicates the analysis, since the graph of total costs becomes discontinuous. Variable costs remain independent of output within the scope of relevance. In fact, their value is presented as a function of the production volume, since the effect of a fall in the maximum productivity of factors takes place. In this regard, under the assumption of independence of fixed costs from the volume of output, variable costs increase with its growth.

Selling price

The assumption that it also remains unchanged is considered the most vulnerable point. This is due to the fact that the selling price depends not only directly on the work of the company, but also on the structure of market demand, the activities of competitors, and so on. The expenses of the enterprise for the promotion of its products, the formation of its trade network, and much more also have a significant impact on the change in the indicator. Here, therefore, it is necessary to investigate the many factors that affect the subsequent assessment. But such an analysis is quite complicated and requires an individual approach in a particular situation.

Other assumptions

The assumption that the services and materials that are used in production remain unchanged is also highly controversial. However, it greatly facilitates the evaluation. There are also the following assumptions:

- Performance does not change.

- There are no shifts in the structure. It makes sense to dwell on this assumption in more detail. Above, the issue of one unit of goods was considered. Accordingly, the problems of distribution of costs for different products, setting their prices, determining the effectiveness of one or another production structure did not arise. In conditions of variability, the assessment requires the use of additional criteria. The break-even point of sales is precisely set only for a specific product output structure.

- Only the quantity of goods produced has a relevant effect on costs. This assumption is of particular importance for analysis. In this case, one should ignore the influence external factors and include in fixed costs all costs that do not depend on the quantity of production.

- Production and sales volumes are equal, or changes in opening and closing stocks are insignificant.

"Sensitivity" rating

The above assumptions are of little use in the real world. However, they can be adapted to reality through sensitivity analysis. This method involves the use of the "what will happen if ..." technique. Within its framework, you can get an answer to the question of how the outcome will change if the originally designed assumptions are not achieved or the situation with them changes. The margin of safety acts as a tool in such an analysis. It represents the amount of revenue that is at a level located below the break-even point. This amount shows the limit to which income can decrease so that there is no minus. Once the underlying assumptions about changes in the original assumptions have been made, the resulting adjustments to the margin of safety and contribution margin need to be established. In management accounting, a continuous assessment of cost behavior is carried out and a break-even point is periodically identified. At its core, sensitivity forms the elasticity of the margin relative to tolerances.

Cost and Price Estimates for Upcoming Periods

The operating firm takes these indicators from its own statistics and the behavior of the cost of production, taking into account the expected changes in the economy. In particular, one should take into account seasonal fluctuations, the activities of competitors, the emergence of substitute products (especially in high-tech markets). New companies cannot draw on their experience because it is not available. For them, therefore, it will be relevant to calculate by analogy with already operating firms in this industry. Along with this, you can use various reference information. The most difficult thing is to create a company that will work in a non-existent sector. In this case, careful costing should be carried out, marketing research. For such firms, it is advisable to use pricing according to the "cost plus" method. The price in this case is obtained by adding a fixed margin to the amount of costs. In this option, the size of marginal income is known, therefore, the break-even point is easily found.

Conclusion

Considering the methods of establishing the break-even point, therefore, it is assumed that the cost of producing a unit of goods and the selling price act as external factors. In other words, by the time the desired indicator is found, these values are known and cannot be changed. The establishment of these key parameters, their deep analysis allows, in turn, to explore the company's break-even planning.

The break-even point is the amount of sales (in quantitative or monetary terms) at which the company operates at zero. With an increase in sales relative to this point, the company will have a profit, and with a decrease, a loss.

What is she for?

This indicator allows you to understand the following already at the planning stage:

- Is it worth investing at current product prices, cost and fixed costs?

- How much do you need to increase sales without changing prices, production costs and fixed costs, so as not to incur losses

- How much it is necessary to sell products for the company to work in plus if one or more of the indicators changes: the price of products, the cost of production, fixed costs of management or production.

Calculation formula

The break-even point in physical terms (pieces, tons, liters, etc.) is calculated by the formula:

BEP (nat.) = FС / (P - AVC), where

- BEP (break-evenpoint) - breakeven point

- FC (Fixed costs) - fixed costs

- AVC (average variable cost) - average variable costs

We note right away that (P - AVC) is, depending on the business, either marginal profit (if this is production) or a margin on goods (if the calculation is done for a store or wholesale trade).

If we want to find the break-even point in monetary terms, then there are two calculation options:

- Find the break-even point in physical terms and multiply it by the price of the product

BEP (den.) = P * BEP (nat.) - Multiply by the price the whole formula for calculating the break-even point. The result is the following formula:

BEP (den.) = P * FC / (P - AVC)

Calculation example for a store

Let's take a simplified situation as an example. The store sells one product - bread at a price of 20 rubles per piece. The store purchases this bread at the factory at a price of 15 rubles per piece. Store fixed costs:

- The seller's salary is 20,000 rubles. + social contributions (34.2%)

- Room rental - 30,000 rubles.

- Utility expenses - 5,000 rubles.

In our example, P = 20 rubles, AVC = 15 rubles, FC = 20,000 * 1.342 + 30,000 + 5,000 = 61,840 rubles.

Substituting these numbers into the formula, we get the following break-even point value in physical terms:

BEP (natural) = 61,840 / (20 - 15) = 12,368

If we want to find the break-even point in monetary terms, then we simply multiply the resulting volume by the price of the product:

BEP (den.) \u003d 12,368 * 20 \u003d 247,360 rubles.

Calculation example for a manufacturing plant

For greater clarity, let's calculate the break-even point at a conditional bakery that supplies bread to retail outlets in the city.

- The price of bread is 15 rubles.

- The cost of production for 1 piece: flour - 7 rubles, water - 3 rubles, packaging - 1 rub.

- General expenses: salary - 50,000 rubles. + deductions (34.2%), depreciation - 30,000 rubles, repair of equipment and premises - 40,000 rubles.

Thus, we get the following values of indicators:

- P = 15 rubles

- AVC \u003d 7 + 3 + 1 \u003d 11 rubles.

- FC = 50,000 * 1.342 + 30,000 + 40,000 = 137,100

The break-even point in physical terms will be equal to:

BEP (nat.) \u003d FС / (P - AVC) \u003d 137 100 / (15 - 11) \u003d 34 275 pieces,

in monetary terms:

BEP (den.) \u003d P * BEP (nat.) \u003d 15 * 34,275 \u003d 514,125 rubles.

The nuances of the calculation

- Unfortunately, the above formula for calculating the break-even point works very well for an enterprise that produces or sells only one product. If your enterprise produces several product names, then the weighted average price for all products and the weighted average cost for all products should be used as the price for the product and the cost price for all products.

Thus, if we, for example, have two products (a loaf and a loaf) and their prices, cost and share in the sales volume are as follows:

- Average variable costs include all costs that are linearly dependent on the volume of production. So, for example, if your wages of production workers directly depend on production volumes (for example, 5 rubles per piece or 5% of revenue), then you need to calculate this cost per unit of output and add it to AVC. In addition, do not forget that taxes on this wages should also be considered as variable costs.

For example, a bakery produces bread and sells it at a price of 20 rubles / kg, and the variable costs for one loaf are as follows: 5 rubles. for flour, 3 rubles. for water, 1 rub. for packaging, 5% of revenue for wages.

In this case, we need to recalculate wages and taxes on it also for one loaf as follows:

Payroll \u003d 20 * 0.05 * 1.342 \u003d 1.342 rubles / loaf, where 20 is the price of the product, 0.05 - 5% of the proceeds, payment to the employee, 1.342 - we increase wages by the amount of social contributions.

Visual display of calculation in Excel

Using the example of calculating the break-even point of a bread store, which we calculated earlier, we will build a calculation graph and calculate the same parameter using Excel tools. Here's what it will look like:

The figure shows that we have calculated the break-even point using four cells. The lower profit calculation table for the store shows that it only comes out of losses when the sales volume becomes equal to 13,000 units (which is more than the calculated 12,368).

The formulas that we used to calculate the indicator can be seen in the following figure:

And the graph below shows the logic of calculating the indicator. In order to turn a profit, our revenue (blue line on the chart) must be greater than fixed (dark blue shading) and variable expenses (light blue shading) combined. The point of intersection of these two graphs is equal to the breakeven point.

Andrei Mitskevich PhD in Economics, Associate Professor of the Higher School financial management Academy of National Economy under the Government of the Russian Federation, head of the consulting bureau of the Institute of Economic Strategies

Break even analysis

The management of the company has to accept various management decisions concerning, for example, the sale price of goods, sales volume planning, the opening of new outlets, increase or, conversely, save on certain types expenses. In order to understand and evaluate the consequences of the decisions made, it is necessary to analyze the ratios of costs, volume and profit.

The break-even analysis shows what happens to the profit when the volume of production, price and basic cost parameters change. The English name for break-even analysis is CVP-analysis (cost - volume - profit, that is, “costs - output - profit”) or Break - even - point (break-even point, break-even point in this case).

Who doesn't know this? However, only a few use the classics in the life of firms. Why? Maybe "professional economics" is so out of touch with life? Let's try to understand what CVP analysis is and why its fate is ambiguous. At least in our country.

Assumptions made in the CVP analysis

Break-even analysis is carried out in the short run under the following conditions in a certain range of production volumes, called the acceptable range:

- costs and output in the first approximation are expressed by a linear relationship;

- productivity does not change within the considered changes in output;

- prices remain stable;

- reserves finished products insignificant.

Academician and our only compatriot - Nobel Prize winner in economics for 1975 L.V. Kantorovich said: “Mathematical economists begin all their work with “suppose that...”. So this cannot be assumed." Perhaps, in our case, the professors stepped on the same rake?

The answer to this question pleases: the hypotheses are working, tested by practice

management accounting. If they are violated, it is not difficult to make changes to the model.

The acceptable range of production volumes (relevance area) is determined by the cost linearity hypothesis. If the hypothesis is not in doubt, the range is accepted as the constraints of the CVP model. Basic classical ratios:

1. AVC ≈ const, i.e. average variable costs are relatively constant.

2. FC are unchanged, i.e. there is no threshold effect.

Then the total cost of producing a product is determined by the relation

TC \u003d FC + VC \u003d FC + a × Q, where Q is the volume of output.

A single-product task lives in textbooks, and a multi-product task lives in practice.

- Single-product tasks answer questions from the field of break-even analysis in the form of the amount of product produced ((2). Most often, CVP analysis in theory comes down to determining the classical break-even point, which shows how many units of production need to be produced to cover all fixed costs. How as a rule, it also applies to the target profit, i.e. it comes down to determining the volume of output that provides a given profit.

- Multi-product tasks answer the same questions in the form of revenue (TC). At the same time, its structure is assumed to be unchanged, at least in the sense of the constancy of the share of marginal profit in revenue.

Accounting methods affect the applicability of CVP analysis. Break-even analysis is carried out using Variable Costing, since Direct Costing and even more so Absorption Costing give errors. If a company does not use at least Direct Costing, then there will be a break-even analysis, therefore one of the reasons for the unpopularity of CVP analysis in Russia is the dominance of Absorption Costing.

Break even points

1) The classical break-even point in terms of the number of units of production assumes the payback of total costs (TC = TC). The critical value is considered to be such a value of sales at which the company has costs equal to the proceeds from the sale of all products (ie, where there is neither profit nor loss).

In a single-product variant, the value of the break-even point (Q b) is directly derived from this ratio:

This formula dominates the literature and, in fact, therefore, has earned the name of the classic break-even point (see Fig. 1).

Rice. 1. Classical CVP-analysis of the behavior of costs, profits and sales volume

An example of calculating the classic break-even point by the number of units of production

The Corporation decides to open several "mini-wholesale" stores. Their characteristics:

- narrow specialization ( office paper, mostly A4 format)

- small trading area(room up to 20 sq.m., or remote outlet);

- minimum sales staff (up to two people);

- form of sales - mostly small wholesale.

Table 1

- Marginal profit per unit of production: 224 -180 \u003d 44 rubles. We calculate the critical point using the formula:

- Break Even Point = Fixed Costs / Profit Margin Per Unit

We get: 10000: 44 = 227.27.To reach the critical point, the store needs to sell 228 reams of paper per month (10 reams per day), with six business days per week.

2) Multi-product break-even analysis. So far, we have assumed that there is one product, but in real life this is a minor special case. Paradoxically, the multicommodity case is less in demand in the literature and even more so in practice. The fact is that in this case the result of the break-even analysis is difficult to interpret. For a practitioner, it is not specific, since it gives hundreds of answers instead of a clear guideline for evaluation.

Let's consider the mathematics of this case. It is clear that the revenue must cover the total costs. In this case, we obtain not one break-even point, but a plane in the N-dimensional space, where N is the number of types of products. If we make a fairly correct and accepted in classical management accounting assumption about the constancy of AVC i \u003d V i , we get a linear equation:

These points, by the logic of reasoning, are very similar to the points of the marginal I breakeven variable. Unfortunately, the remaining inseparable fixed costs cannot be distributed between products on the same and balanced bases. If all products are cash cows, such a base could be the notional contribution margin (revenue minus variable costs minus each product's own fixed costs). But since output is unknown in the break-even point question, neither the notional contribution margin nor the revenue work.

In the second step, you will have to allocate the remaining costs:

NFC = FC - ΣMFC i

Options:

a) equally, if there is no reason to prefer any one product;

b) in proportion to the planned revenue, if the sales plan is drawn up. Naturally, only the total fixed costs are shared;

c) if you have a plan, you can return to a balanced base (for example, marginal profit), but without part of the production

attributed to cover own costs (MPC i).

An example of calculating break-even points based on the developed Direct Costing.

Suppose a firm produces two types of products: "Alpha" and "Beta", sold at a price of 9 and 20 thousand dollars apiece, respectively. Average Variable Costs (AVC) are planned at $4,000 and $10,000 respectively.

Individual fixed costs for Alpha were $2,000,000 for the planned quarter, and for Beta, $8,000. The remaining fixed costs (NFC) turned out to be $10,000.

a) when dividing undivided fixed costs equally (5000 per type of product), we get:

Let's try to determine the break-even points in different ways. First, we calculate the coverage of our own fixed costs:

b) when dividing in proportion to the plan, you need to know this plan: 2900 and 2175, for example, in pieces. As the distribution base, we take the proceeds minus the coverage of own fixed costs:

22500 thousand dollars \u003d 2900 x 9 - 400 x 9 for Alpha;

$27,500 = 2175 x 20 - 800 x 20 for Beta.

c) the marginal profit base assumes that the planned output is reduced by the amount of own coverage (in units):

2900 — 400 = 2500 2175 — 800 = 1375

Conclusion: the deviations in the calculations are small, so you can use any of the proposed methods in the case of an approximate equality of the volumes of products. Otherwise, it's better to use methods B and C:

B - for growing markets and products;

B - for "cash cows".

3) The classical break-even point in terms of revenue is the most common approximate solution to a multi-product problem. It is assumed that the revenue structure changes insignificantly. The task is set as follows: to find such a value of revenue at which profit is zeroed. To do this, the economist requires a coefficient ( to), showing the share of variable costs in revenue. It is not difficult to find it, knowing the share of variable costs in total costs and profit in revenue. As a result, we get the equation:

For example:

- share of variable costs in revenue = 9742/16800 = 58%;

- fixed costs = 5816 thousand rubles;

- break-even point \u003d 5816 / (1-0.58) \u003d 13848 thousand rubles of revenue

In contrast to the classical break-even point in terms of the number of units of production, here it is necessary to make a reservation regarding the accuracy of the results:

- formula (7) is certainly correct with the same output structure;

- however, a less stringent condition can also be formulated: the invariance of the coefficient k, i.e. share of variable costs in revenue.

- Break-even point based on margin ordering in descending order. The break-even point shifts to the left when using the ordering of products in descending order of marginal profit.

Let's consider this interesting and rarely described effect with an example. So, the firm has fixed costs equal to $16,000 and produces 4 products with different shares of marginal profit in revenue (see Table 2).

Table 2. Initial data for calculating the break-even point based on marginal ordering

|

Product |

Revenue (TK) Doll. |

Marginal profit (/OT), USD |

Share of contribution margin in revenue |

|

Calculate the break-even point for revenue based on formula (7):

Let's determine it taking into account that we will first produce the most profitable products: A and B. They are just enough to cover fixed costs: μπ(A) + μπ(B) = 12000 + 4000 = 16000 = FС. Thus, we obtain an optimistic estimate of the break-even point:

20000 + 8000 = 28000.

The break-even point based on ascending margin order gives a pessimistic estimate. Let's use the same example to illustrate. Products D, C, B are only enough to cover $12,000, and the remaining fixed cost of $4,000 is one third of the output of product A. That is, a pessimistic estimate of the break-even point:

Break-even points based on marginal descending and ascending ordering together give an interval of possible break-even points.

4) Point 1. LCC break even. The Life Cycle Costing approach to the problem of cost and profit defines the break-even point as an output that pays for the full costs, taking into account the entire life of the product. The LCC approach encroaches on the prerogatives of investment design. In addition to fixed costs, he also insists on covering investment costs.

An example of an LCC analysis

Suppose a consortium Russian firms invested $500 million in research and development (R&D) of the new aircraft.

Fixed costs consist of $700 million in R&D (a one-off cost in a given year) plus $50 million in annual fixed costs. Variable cost per aircraft - $10 million. It is expected that 25 aircraft will be produced per year, and they can be sold on the market for a maximum of $16 million. How many planes need to be sold to offset all costs without taking into account the time factor (this is also a break-even point, but taking into account what?) and how many years will it take?

Solution: Let's denote the unknown number of years as Y. Fixed costs will depend on the number of years the break-even point is reached: 700 + 50 x Y. Equate the total costs and revenue for Y years:

700 + 50 x Y + 25 x 10 x Y = 25 x 16 x Y.

Hence Y = 7 years, during which 175 aircraft will be produced and sold.

5) Marginal break-even point (payback point for an additional unit of output). In modern complex production, marginal costs (for producing an additional unit of output) do not immediately become lower than the price. Release,

providing break-even of an additional unit of production, is determined by the ratio:

Q bm: P \u003d MS (Q bm) (8)

This point shows the moment (output) when the company starts to work "in plus", i.e. when with the release of one more unit of production, profits begin to grow.

Unfortunately, there is no more detailed formula. This ratio

6) Break-even point of variable costs (point of coverage of variable costs):

TR = VC or P = AVC. (nine)

It shows that the process of recoupment of fixed costs will soon begin. This is an important indicator both for managers who “started” New Product as well as for owners. However, there is no more intelligible formula for calculations here either. The reason is the same: the ratio

(9) always individually.

Target profit points

They show the output of a single product (or revenue - in the case of multi-product production), providing a given mass or rate of return.

1. Target profit point by the number of units of production.

The traditional indicator is the output that provides the target profit. Similar calculations are performed in many firms. Suppose the required profit is π, that is,

This formula is easily modified in the case of a target after-tax profit. Here are the simplified calculations. If the target profit after tax should be equal to z, then (TR - TC) × (1 - t) = z, where t is the income tax rate. Therefore, (P - AVC) x Q x (1 - t) = z + FC × (1 - t) or

2. The target profit point for revenue is easily calculated by analogy with formula (7):

In the multicommodity case, it is subject to the same restrictions on the invariance of the coefficient k, i.e. share of variable costs in revenue.

Sensitivity analysis is based on the use of the “what happens if one or more factors that affect the amount of sales, costs or profits” change. Based on the analysis, you can get data about the final result with a given change in certain parameters. The sensitivity analysis is based on safety edges.

Safety edges (sometimes translated as safety margin or safety margin) show the margin of safety, break-even business as a percentage or natural units, or in rubles of revenue. The percentage representation is more visual and, most importantly, allows you to normalize this important indicator. Although these norms are extremely approximate, they are useful. Mathematicians speak of such figures and formulas with disdain: "management indicators." But this “engineering approach” cannot be avoided.

Classic safety edge by number of units:

It shows how much percentage revenue can decrease with break-even production. Less than 30% is a sign of high risk.

Classic Safety Edge by Revenue:

Both of these safety margins are good for the business as a whole, as fixed costs are understandable, but not very useful for business segments. However, the "frontal" application of variable or marginal costs, as you remember, requires the non-linearity of their functions. Classical management accounting does not study these functions and therefore is forced to consider them linear. Does this mean that there are no other safety edges than the classic ones? The answer will be negative.

The price safety margin shows how much price needs to be lowered in order for the profit to become zero. This will be at the critical price P k = AC. Then the margin of safety will be as a percentage of the current price:

The variable cost safety margin shows how much the unit variable costs need to increase in order for the profit to go to zero. The critical value of AVC is reached at AVC = P - AFC. That's why

The margin of safety for fixed costs in absolute terms is equal to profit, and in relative terms:

Please note that in formulas (15-17) the output remains unchanged.

Problems in determining break-even points

If a firm faces semi-fixed costs, there may be multiple break-even points. The break-even chart (see Figure 2) shows three break-even points, and profit and loss zones follow each other as the volume of activity increases.

Rice. 2. Multiplicity of classical break-even points in the case of semi-fixed costs.

Similar reproduction also applies to non-classical break-even points.

Difficulties in conducting a break-even analysis may be due to the following reasons:

- if supply is high, the unit price may have to be lowered. Consequently, a new break-even point will appear, lying to the right;

- "Large" buyers are likely to be eligible for volume discounts. The break-even point shifts to the right again;

- if demand exceeds supply, it may be appropriate to increase the price. This will move the break-even point to the left;

- the cost of raw materials and materials per unit of production may decrease with large volumes of purchases or increase with supply interruptions;

- the unit cost of wages of production workers is likely to decrease with a large volume of production;

- both fixed and variable costs tend to increase over time;

- costs can not always be accurately divided into fixed and variable;

- the structure of sales can change quite significantly.

Primitive business plans simply ignore all these elementary analytical calculations.

However, it is believed that break-even analysis is carried out everywhere and its value is great. My observations do not support this. Like any model, the CVP has its own “battlefield”, and it is fragmented. Many firms conduct CVP analysis only for new projects. Unfortunately, regular work with the profitability of products and segments in our country is still not enough.

Case with solutions

So, two firms: CJSC "Staromehanicheskij Zavod" (hereinafter - SMZ) and OJSC "Foreign Automation" (hereinafter - ZAM) work in the Little Russian market and manufacture a part used in car repairs. Today the two companies have divided Russian market- each holds 50%. Manufactured parts have the same quality and price. The production facilities of both companies are located in the vicinity of Mariupol.

However, companies differ radically in their cost structure. "Foreign Automation" has a fully automated and very capital-intensive production. And the "Old Mechanical Plant" is a non-automated production with a large share of manual labor. Monthly profit and loss statements of companies are as follows (see table 1).

Table 1. Initial situation (in c.u.)

|

Indicators |

"Foreign Automation" |

"Old Mechanical Plant" |

|

Sales, pcs. | ||

|

Price for one | ||

|

Unit Variable Costs | ||

|

Unit fixed costs | ||

|

Total unit cost | ||

|

Full costs |

9.5x5000 = 47500 |

9.5x5000 = 47500 |

|

50000 — 47500 = 2500 |

50000 — 47500 = 2500 |

Both companies are looking at ways to increase profits. One of them is to start selling your products to a large, but relatively low-income (or economical) segment of buyers, which in this moment no one is serving. The potential capacity of this segment is 2000 pieces per month. Thus, the company that has captured this segment, sales in physical terms will increase by 40%. The only problem is that in this segment, consumers will buy parts at a price no higher than 8.50 USD. e. per piece, i.e. 15% lower than the market price and 1 c.u. That is, below the total cost of production at the moment. How can you sell below cost? - the head of the FEO with many years of experience at the "Old Mechanical Plant" is indignant.

Question 1: Let's say both companies can cost-free segment the market (i.e. start selling parts to the economy segment at a 15% discount without undermining their full-price sales to wealthy customers). To what extent can each company increase profits if it increases sales (in units): a) by 20%, that is, by capturing half of the economy segment?

b) by 40%, capturing the entire economy segment?

Should companies (one or both) use this opportunity to increase profits?

|

Question |

Response Logic |

"Foreign Automation" |

"Old Mechanical Plant" |

|

Profit increment (Δπ) is calculated through the marginal profit per unit of production in an additional batch (αμπ) |

αμπ \u003d 8.5 - 2.5 \u003d 6 Δπ \u003d 6x1000 \u003d 6000 |

αμπ \u003d 8.5 - 5.5 \u003d 3 Δπ \u003d 3x1000 \u003d 3000 |

|

|

αμπ \u003d 8.5 - 2.5 \u003d 6 Δπ \u003d 6x 2000 \u003d 12000 |

αμπ \u003d 8.5 - 5.5 \u003d 3 Δπ \u003d 3x2000 \u003d 6000 |

||

Conclusion: Both companies will be happy to "grab" even half of the economy segment, not to mention the happiness of taking possession of it entirely.

Question 2: What if neither SMZ nor ZAM can effectively segment the market, and both firms will be forced to set a single price for all buyers (i.e. 8.50 USD for both the economy segment and wealthy buyers ).

a. Calculate the BOP (break even sales volume) for each

companies, if the price is reduced to 8.50 c.u. e.

b. How much would each company's profits increase if its sales

increase by 40% (in pieces)?

Attention: BOP (break-even sales volume) in this case assumes that the company should receive the same, not zero, profits.

Breakeven sales volume is more common in practice than the classic CVP analysis. In life, it is found, in textbooks - not always. This is a variant of the target profit point in dynamics: when factors change, the profit remains at the same level. The break-even volume of sales assumes that the company should receive the same profits during changes, and not zero. For example, an old machine has been replaced with a more efficient and expensive one. Naturally, the question arises, how much should output be increased in order to “recoup costs”?

|

Question |

Response Logic |

"Foreign Automation" |

"Old Mechanical Plant" |

|

|

Calculated through the equality of marginal profits before and after changes |

μπ (up to) \u003d 7.5x5000 \u003d 37500 \u003d μπ (after) = 6xQ μπ (after) = 7.5x5000 =37500 |

μπ (up to) \u003d 4.5x5000 \u003d 22500 \u003d μπ (after) = 3xQ |

||

|

b. Output growth by 40% |

Profit growth (Δπ) is calculated as the difference between marginal profits before and after changes |

μπ (after) \u003d 6x7000 \u003d 42000 μπ \u003d 42000 - 37500 \u003d 4500 |

μπ (after) = 4.5x5000 = 22500 |

|

This is what we call cost structure competitiveness with lower average variable costs. Foreign Automation will survive the price cuts, but Old Mechanical Plant will not. Dumping (the game to lower prices) is the lot of firms with low variable costs. There are no fixed costs here.

Question 3: While the companies were thinking, their market was invaded by a strong competitor - "Avtomobilny Zavod". He easily captured half the market, trading the same parts for $9. We will have to return to the original situation and analyze the reliability of the SMZ and ZAM. Both firms lost half of their sales (in units). The results are presented in table. 2.

Table 2. The situation after the invasion of the "adversary" (in c.u.)

|

Indicators |

"Foreign Automation" |

"Old Mechanical Plant" |

|

Sales, pcs. | ||

|

Price per piece e. | ||

|

Specific | ||

|

variables | ||

|

costs | ||

|

Fixed costs (per month) | ||

|

Specific | ||

|

permanent |

14 = 35000: 2500 | |

|

costs | ||

|

Total unit cost | ||

|

Full costs |

16.5x2500 = 41250 |

13.5x2500 = 33750 |

|

22500 — 41250 = -18750 |

22500 — 33750 = -11250 |

Of course, both companies are at a loss, but it is perhaps easier to transfer them to the Staromehanicheskoy Zavod. This is what we call cost structure reliability with lower fixed costs.

Question 4: Morning. The invasion of the "Automobile Factory" turned out to be a nightmare. Given that no single company can segment the market, what advice would you give each company on this opportunity?

Answer: "Foreign Automation" should lower the price, but "Old Mechanical Plant" - no. ZAM has every chance to win price competition due to lower variable costs.

After analyzing the situation, ZAM decided to take the opportunity to sell parts to a new segment and reduced prices by 15%. Its sales rose to 7,000 units per month at a price of $8.50. e. Belatedly, SMZ was also forced to cut prices to keep its customers. SMZ management believes that if they had not reduced their prices, they would have lost 60% of sales. Unfortunately, after the price reduction, SMZ operates at a loss.

Question 5: Was Staromekhanichesky Zavod's decision to cut prices financially sound? For example, if SMZ decides to leave this market entirely, it can cut its fixed costs in half. For example, refuse to rent premises, land and other expenses. The remaining 50% of fixed costs is servicing a bank loan for the purchase of equipment that has a zero salvage value. Calculate and compare profits for different options.

Position after price reduction:

μπ (up to) \u003d 4.5x5000 \u003d 22500

μπ (after) = 3x5000 = 15000

FC = 20000, π = -5000.

Alternative option: do not reduce the price, but lose part of the market:

μπ (up to) \u003d 4.5x5000 \u003d 22500

μπ (after) \u003d 4.5x2000 \u003d 9000

FC = 20000, π = -11000.

Therefore, price reduction is beneficial in the short run.

When leaving the market, π = -10000. Therefore, one should stay and reduce the price, although production will be unprofitable: FC = 20000, π = 15000 - 20000 = -5000.

Fortunately, the managers of the Old Machine Factory read Michael Porter's book " Competitive advantages and decided to analyze how the entire value chain works. As a result of market analysis, they found that at least 3,500 parts are bought monthly by drivers, who then have to remake this part on their own so that it better suits their brand of car: namely, the Volga. Thus, there is an opportunity on the market to produce a specialized version of the part for this category of drivers. And although the cost of production at the LMP will increase, the additional costs will still be less than what drivers currently spend on reworking the part.

For the production of specialized parts, SMZ will have to invest additional capital, the fee for which will be 3000 c.u. per month.

Question #6: In order to produce specialized parts, SMZ would have to buy new equipment and a new building, which would cost $23,000. fixed costs per month instead of 20,000 c.u. e. per month. The plant management is convinced that they will be able to sell specialized parts for 6 cu more than conventional parts (ie 16 cu), but the unit variable costs will increase by 3.00 cu. e. per month. Would it be beneficial for SMZ to focus on the production of only specialized parts?

Answer: FC \u003d 23000, π \u003d (1b-8.5) x3500 - 23000 \u003d 3250. Yes, the manufacture of only specialized parts is profitable, since the profit will increase by 3250 - 2500 \u003d 750 c.u. e.

Question #7: What is the minimum number of custom parts that SMZ must sell per month to exceed the profits it currently earns as a generic parts manufacturer? Remember? This is what we call break-even sales volume.

Answer: FC \u003d 23000, π \u003d (16-8.5) xQ - 23000 \u003d 2500. Q \u003d 3400.

Question No. 8: How much will the profits of Staromehanichny Zavod as a manufacturer of specialized parts increase if it sells 3,500 pieces per month at a price of 16 USD per piece. ?

Answer: 3250 — 2500 = 750.

"Unfamiliar options for break-even analysis"

There are other options for break-even analysis. For most, they will be unexpected. We call them "three break-even points":

The first and fastest achievable - the marginal break-even point - shows at what output the price will begin to recoup the additional costs of producing one more unit of output (P > MC - in conditions of perfect competition or MR > MC - in conditions of imperfect competition). The first condition (P > MC) corresponds to the spirit of management accounting and is quite worthy to use. The second (MR > MC) is suitable only for pure economic theory, although it would be presumptuous to deny the possibility of its practical use.

The second point - the break-even point of variable costs - shows the output at which it will be possible to cover all variable costs (TR\u003e VC). Naturally, such a statement of the problem is typical for Variable Costing. In the case of using Direct Costing, a similar point will be called the break-even point of direct costs (TR> DC).

The third point - classical - sets the output at which it will be possible to cover all costs (TR\u003e TC). It has filled all the textbooks, so most students and professionals think that the classic break-even point is CVP analysis. This is a clear exaggeration, or rather an underestimation of the role and capabilities of CVP analysis.

Example. Evaluation of the work of company stores and allocation of general administrative costs

At the beginning of the year, a large Moscow company set an ambitious goal: to open 200 new branded stores across the country in a couple of years. The central office economist asked how to allocate the costs of the central office between stores? The answer, surprisingly, relies on the “three break-even points”:

1. Again open shop must first pay off its current content. This is the first and concrete task for management. It is not necessary to post costs to such stores. This is also a marginal break-even point, but not for products, but for stores. Ceteris paribus, the team that gets through the first stage faster will “win the capitalist competition.” Moral incentives have not been canceled.

2. As soon as the store contributes to the coverage, another stage of development will begin. Here it is required to recoup the accumulated current losses of the previous stage. This is also a kind of break-even point for variable costs, but not for products, but for stores.

3. Only at the next, third stage, it is necessary to fight for the classic payback. And only here you can distribute the costs of the central office between stores. Advanced Direct Costing welcomes this solution, but does not give advice on which explode bases indirect costs use.

It is on such a decision that the business plan of each store or branch, representative office, business area, and so on should be aimed.

The breakeven point shows a certain amount Money, which, as a result of its work, an enterprise or a trademark receives, and at the same time it is able to cover all existing costs, namely fixed and variable.

Fixed costs do not directly depend on the number of products or services provided and include:

Dear reader! Our articles talk about typical ways to resolve legal issues, but each case is unique.

If you want to know how to solve exactly your problem - contact the online consultant form on the right or call by phone.

It's fast and free!

- wages, namely management;

- rent of production areas and equipment;

- property taxes;

- deductions for depreciation;

- payment for security services.

Variable costs are dependent on the production process, on the volume of products and services rendered. These should include:

- payment for utilities;

- salary deductions for full-time workers;

- costs associated with the purchase of fuel;

- purchase of basic and component materials;

- the cost of purchasing raw materials.

It should be noted that if the company fully and without any problems pays off the received invoices, then it works without losses and has the amount of money that is called the break-even point. It can be presented in calculations both in monetary terms and in units of sold or manufactured products.

Calculation options

To find the break-even point, you need to follow several steps, namely:

- collection of information on the volume of production, the number of products sold, the presence or absence of profit and loss;

- determination of the amount of fixed and variable costs;

- calculation of the break-even point and certain safety zones;

- conclusion based on the data obtained, with the help of which it is possible to estimate the level of sales and the optimal volume of production that will provide financial stability companies;

The analytical method implies the calculation of such a volume of production, in the implementation of which the income will cover all existing costs, namely, the profit in this case should be equal to zero. When using this method, one should take into account information on the sale of all manufactured products, that is, what was produced, then sold without residues.

The graphical method involves the construction of a graph with two axes X and Y, on which, respectively, the volume of manufactured products is plotted, and revenue with variable, fixed and production costs. The point at the intersection of costs and sales proceeds is called break-even.

How to calculate

Any calculations should be carried out based on the values of one period of time, for example, it can be a year, half a year, a quarter, a month. It is also necessary to take into account the type of activity of the institution. Here are the break-even point formulas for a store, enterprise, and production.

An enterprise that carries out trade has more than 1000 units of products, in this regard, in order to search for turnover at the break-even point Accounting uses the formula:

Tb = (Z total / %R) * 100%.

Where, Z total - total costs

%R - percentage of profitability, determined by the ratio of cost and unit price.

The search for a break-even point for an enterprise begins with determining profit using the formula:

P = V– Z DC – Z AC

Where, P - profit,

V - sales proceeds,

Z post - fixed costs,

Z variable - variable costs.

Accordingly, the revenue from the sale of services can be calculated using the following formula:

V = P + Z DC + Z AC

Since the profit at the break-even point is equal to zero, then the revenue formula will be as follows:

V = Z DC + Z AC or

C * Tb = Z DC + Z AC * Tb.

Hence, Tb in physical terms is calculated by the formula:

Tb = Z post / (C - Z variable).

Where, C is the unit price.

And Tb in monetary terms:

Tb = V * Z DC / (V - Z AC).

Calculation example

Shop "Plyushka" is a trading company that sells bakery products of the firm "Bread". The goods are provided in a wide range of more than 2000 items. The average price for bakery goods is 44 rubles.

The rate of profitability sales established by the enterprise is 52%. At the same time, fixed costs are 48,000 rubles, and include payment for rent in the amount of 25,000 rubles, for advertising - 5,000 rubles, and variable costs for staff salaries amount to 18,000 rubles.

Tb \u003d (48000 / 52%) * 100%,

Tb = 92307 rubles.

To determine the payback of the project (Op) of the store, you should divide Tb / C from the average, from here, respectively:

From this it follows that for effective and paid back work it will be enough if 2098 customers come to the store to buy bakery goods in a month.

The calculation of the break-even point for the Khleb enterprise, which produces bakery products, is carried out on the basis of the proposed data. The average price for products is 36 rubles, variable costs per unit are 8 rubles, fixed costs are 120,900 rubles, 3,000 items are produced per month. The proceeds from the sale is 108,000 rubles.

To calculate the break-even point of an enterprise, it is necessary to use the formula in monetary terms Tb \u003d V * Z post / (V - Z variable):

Tb = 108000 * 120900 / (108000 - 24000),

Tb = 13057200000 / 84000,

Tb = 155443 rubles.

The received 120908 rubles mean that the company will receive zero profit if it produces products for the calculated amount.

The break-even point for production will be calculated by the formula Tb = Z post / (C - Z variable) in physical terms:

Tb \u003d 120900 / (36 - 8),

Tb = 120900 / 28,

Tb = 4318 pieces.

Taking into account the data obtained, it should be concluded that the company needs to increase production to 4318 units, having reached this volume, the profit will be equal to zero.

How to Calculate Break Even Point in Microsoft Excel

Complex and voluminous economic calculations, for convenience it should be done in Excel. To do this, it is enough to enter the appropriate formulas to get the result.

Schedule

Building a break-even chart is an integral part of the calculations. It clearly shows the efficiency of work, profit and loss.

Building a break-even point based on analytical calculations of the store, enterprise and production in Excel will look like this:

For enterprises, firms and others legal entities, the calculation of the break-even point is an important criterion for evaluating their activities. Analytical data reflects the feasibility of doing business and possible adjustments in case of non-receipt of profit.

The essence of the calculations performed is revealed when constructing a graph on which, in more and all the necessary information is clearly displayed, with the help of which it is possible to draw conclusions. It includes the volume of production, all existing costs, both in kind and in monetary terms.

To understand the information presented on the graph, maybe not only a specialist in the field of economics. This is due to the fact that the area above the breakeven point always indicates a profit and vice versa. With this data, it is possible to make changes in the policy of production or provision of services. And also in the Microsoft Excel program, it is possible to predict future changes before translating them into reality.